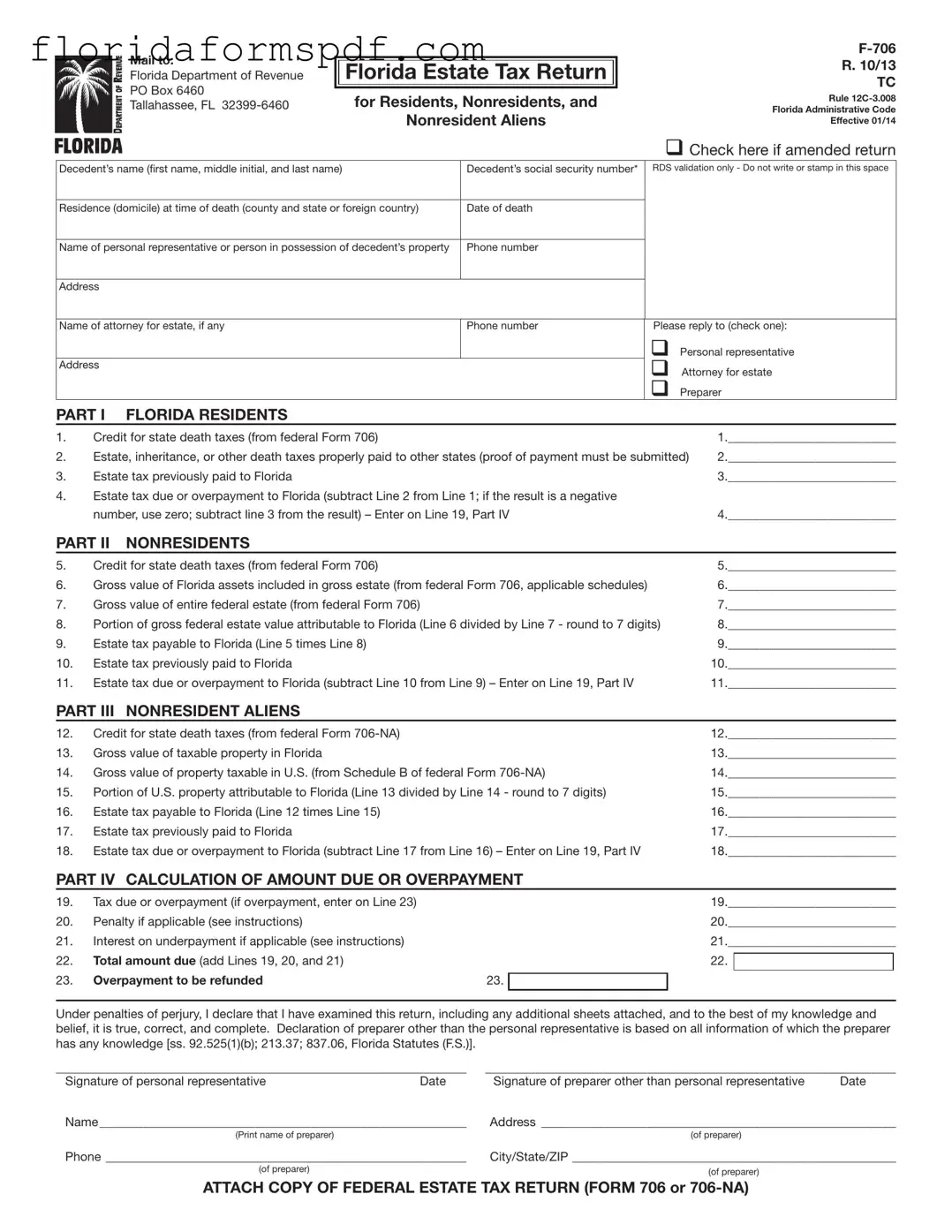

Fill Out a Valid Florida F 706 Template

When dealing with the aftermath of a loved one's passing, navigating the legal and financial responsibilities can be overwhelming, particularly concerning estate taxes. In Florida, the handling of these taxes for residents, nonresidents, and nonresident aliens is encapsulated within the Florida F 706 Form, formally known as the Florida Estate Tax Return. This critical document, required under specific conditions outlined by the Florida Department of Revenue, serves as the primary means to reconcile state estate tax obligations with the federal credit for state death taxes. Its necessity hinges on factors such as the decedent's date of death, with distinct protocols for filing, payment, and possibly obtaining extensions mirroring those of the Internal Revenue Service. The form demands detailed information on the decedent, including social security numbers and residence at the time of death, while also accommodating the potential to amend returns should changes to the corresponding federal estate tax return occur. Further, it addresses penalties and interest for late payments, underscoring the importance of adhering to deadlines. Essential to the proper settlement of the decedent's estate, the F-706 ensures compliances, such as the payment of taxes due to the state or the securing of refunds for overpayment, thereby playing a pivotal role in the estate administration process.

Document Preview Example

Mail to:

Florida Department of Revenue

PO Box 6460

Tallahassee, FL

|

||

Florida Estate Tax Return |

R. 10/13 |

|

TC |

||

|

||

for Residents, Nonresidents, and |

Rule |

|

Florida Administrative Code |

||

|

||

Nonresident Aliens |

Effective 01/14 |

q Check here if amended return

Decedent’s name (first name, middle initial, and last name) |

Decedent’s social security number* |

RDS validation only - Do not write or stamp in this space |

|

|

|

Residence (domicile) at time of death (county and state or foreign country) |

Date of death |

|

|

|

|

Name of personal representative or person in possession of decedent’s property |

Phone number |

|

|

|

|

Address |

|

|

|

|

|

Name of attorney for estate, if any |

Phone number |

Please reply to (check one): |

|

|

q Personal representative |

Address |

|

q Attorney for estate |

|

|

|

|

|

q Preparer |

PART I FLORIDA RESIDENTS

1. |

Credit for state death taxes (from federal Form 706) |

1.___________________________ |

2. |

Estate, inheritance, or other death taxes properly paid to other states (proof of payment must be submitted) |

2.___________________________ |

3. |

Estate tax previously paid to Florida |

3.___________________________ |

4.Estate tax due or overpayment to Florida (subtract Line 2 from Line 1; if the result is a negative

|

number, use zero; subtract line 3 from the result) – Enter on Line 19, Part IV |

4.___________________________ |

|||||

PART II |

NONRESIDENTS |

|

|

|

|

|

|

5. |

Credit for state death taxes (from federal Form 706) |

|

|

5.___________________________ |

|||

6. |

Gross value of Florida assets included in gross estate (from federal Form 706, applicable schedules) |

6.___________________________ |

|||||

7. |

Gross value of entire federal estate (from federal Form 706) |

|

|

7.___________________________ |

|||

8. |

Portion of gross federal estate value attributable to Florida (Line 6 divided by Line 7 - round to 7 digits) |

8.___________________________ |

|||||

9. |

Estate tax payable to Florida (Line 5 times Line 8) |

|

|

9.___________________________ |

|||

10. |

Estate tax previously paid to Florida |

|

|

10.___________________________ |

|||

11. |

Estate tax due or overpayment to Florida (subtract Line 10 from Line 9) – Enter on Line 19, Part IV |

11.___________________________ |

|||||

PART III |

NONRESIDENT ALIENS |

|

|

|

|

|

|

12. |

Credit for state death taxes (from federal Form |

|

|

12.___________________________ |

|||

13. |

Gross value of taxable property in Florida |

|

|

13.___________________________ |

|||

14. |

Gross value of property taxable in U.S. (from Schedule B of federal Form |

14.___________________________ |

|||||

15. |

Portion of U.S. property attributable to Florida (Line 13 divided by Line 14 - round to 7 digits) |

15.___________________________ |

|||||

16. |

Estate tax payable to Florida (Line 12 times Line 15) |

|

|

16.___________________________ |

|||

17. |

Estate tax previously paid to Florida |

|

|

17.___________________________ |

|||

18. |

Estate tax due or overpayment to Florida (subtract Line 17 from Line 16) – Enter on Line 19, Part IV |

18.___________________________ |

|||||

PART IV CALCULATION OF AMOUNT DUE OR OVERPAYMENT |

|

|

|

||||

19. |

Tax due or overpayment (if overpayment, enter on Line 23) |

|

|

19.___________________________ |

|||

20. |

Penalty if applicable (see instructions) |

|

|

20.___________________________ |

|||

21. |

Interest on underpayment if applicable (see instructions) |

|

|

21.___________________________ |

|||

22. |

Total amount due (add Lines 19, 20, and 21) |

|

|

22. |

|

|

|

|

|

|

|

||||

23. |

Overpayment to be refunded |

23. |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of perjury, I declare that I have examined this return, including any additional sheets attached, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer other than the personal representative is based on all information of which the preparer has any knowledge [ss. 92.525(1)(b); 213.37; 837.06, Florida Statutes (F.S.)].

__________________________________________________________________ |

__________________________________________________________________ |

||

Signature of personal representative |

Date |

Signature of preparer other than personal representative |

Date |

Name___________________________________________________________ |

Address _________________________________________________________ |

||

(Print name of preparer) |

|

(of preparer) |

|

Phone __________________________________________________________ |

City/State/ZIP ____________________________________________________ |

||

(of preparer) |

|

(of preparer) |

|

|

|

|

|

ATTACH COPY OF FEDERAL ESTATE TAX RETURN (FORM 706 or

INSTRUCTIONS FOR FORM

R.10/13 Page 2

General Information

Florida’s estate tax is based on the allowable federal credit for state death taxes. Florida tax is imposed only on those estates subject to federal estate tax filing requirements and entitled to a credit for state death taxes (Chapter 198, F.S.). Estate tax is not due if a federal estate tax return (Form 706 or

Form

The requirement to file Form

Date of Death |

|

|

|

On or before December 31, 2004 |

Yes** |

|

|

On or after January 1, 2005 |

No |

|

|

**If required, Form

Due Dates and Extensions of Time

Form

us within 30 days of mailing the request and 30 days of receiving the federal approval. An extension of time to file does not extend the time to pay. Interest accrues on the Florida tax due from the original due date until paid.

Tax Paid to Other States

For Florida residents: if estate, inheritance, or other death taxes were properly paid to other states, proof of payment must be submitted to the Florida Department of Revenue. (Proof of payment means the final certificate of payment showing the specific amounts of tax, penalty, or interest assessed and paid.)

*Social Security Numbers

Social security numbers (SSNs) are used by the Florida Department of Revenue as unique identifiers for the administration of Florida’s taxes. SSNs obtained for tax administration purposes are confidential under sections 213.053 and 119.071, Florida Statutes, and not subject to disclosure as public records. Collection of your SSN is authorized under state and federal law. Visit our Internet

site at floridarevenue.com and select “Privacy Notice” for more information regarding the state and federal law governing the collection, use, or release of SSNs, including authorized exceptions.

Where to File

Mail your completed

Tallahassee, FL

If you are requesting a nontaxable certificate, include the $5.00 fee.

Signature

The personal representative must sign the return declaration under penalties of perjury. If someone else prepares the return, the preparer must also sign the return.

Amending Form

If you must change a return that has already been filed, you must complete another Form

Penalties and Interest

Penalties – If tax is not paid by the due date (or approved extension date) a late payment penalty of 10% of the unpaid tax is due. After 30 days, the late penalty increases to 20%. An added penalty of 10% per month up to a maximum of 50% of the tax due is imposed if the unpaid tax is due to negligence or intentional disregard. A fraud penalty of 100% of the tax due is imposed if the unpaid tax is due to willful intent to defraud. However, the Department of Revenue is authorized to compromise or settle these penalties pursuant to section 213.21, F.S.

Interest – Interest is due on late payments from the due date until paid. Interest rates are updated January 1 and July 1 of each year. To obtain current interest rates, visit our website at floridarevenue.com.

Need Assistance?

Information and forms are available on our Internet site at

floridarevenue.com.

If you have any questions, you may contact Taxpayer Services at

For a written reply to your tax questions, write:

Taxpayer Services MS

Florida Department of Revenue

5050 W Tennessee St

Tallahassee, FL

For federal estate tax information or forms, visit the IRS website at www.irs.gov.

Document Overview

| Fact Name | Detail |

|---|---|

| Form Title | F-706 Florida Estate Tax Return |

| Revision Date | October 2013 (R. 10/13) |

| Governing Law | Rule 12C-3.008 Florida Administrative Code; Chapter 198, F.S. |

| Purpose | Used for residents, nonresidents, and nonresident aliens to report Florida estate tax |

| Who Must File | Estates of decedents with date of death on or before December 31, 2004, required to file a federal estate tax return |

| Filing Deadline | Due within 9 months after the decedent's death |

| Extension of Time | Florida grants the same extension provided by the IRS, with proof of federal extension required |

| Penalties and Interest | Penalties for late payment and interest accrues from the original due date until payment is made |

| Amended Return | To amend, complete another F-706 and check the amended return box |

| Where to File | Mail to: Florida Department of Revenue PO Box 6460 Tallahassee, FL 32399-6460 |

| Social Security Numbers | Used as unique identifiers for tax administration, confidential under Florida law |

Instructions on How to Fill Out Florida F 706

Filing out the Florida F-706 form is an important process that ensures compliance with estate tax requirements for residences, nonresidents, and nonresident aliens with assets connected to Florida. Once completed appropriately, this document provides crucial information to the Florida Department of Revenue concerning estate taxes due or overpayments from the decedent's estate. The steps to fill out the form are straightforward, provided all the necessary information is at hand, including any relevant federal estate tax returns.

- Begin by obtaining the Florida F-706 form from the Florida Department of Revenue's official website or office.

- Enter the decedent's full name, including the first name, middle initial, and last name, in the designated space at the top of the form.

- Fill in the decedent’s social security number without making any marks or stamps in the space reserved for RDS validation.

- Specify the residence (domicile) of the decedent at the time of death, including the county and state or foreign country.

- Input the date of the decedent’s death.

- Provide the name, phone number, and address of the personal representative or the person in possession of the decedent’s property.

- If applicable, insert the name and contact information of the attorney for the estate.

- Indicate the appropriate contact preference by checking either the personal representative, attorney for the estate, or preparer box.

- In Part I, for Florida residents, enter the credit for state death taxes from federal Form 706, and fill out lines 2 through 4 as instructed on the form.

- In Part II, for nonresidents, enter the necessary information from lines 5 through 11 based on federal Form 706 details and calculations provided in the instructions.

- For nonresident aliens in Part III, input the required details from lines 12 through 18, utilizing information from federal Form 706-NA as instructed.

- In Part IV, calculate the total estate tax due or overpayment following the lines 19 through 23 instructions.

- The personal representative must sign and date the form. If another individual prepares the form, their signature, name, address, phone number, and city/state/ZIP also need to be included.

- Attach a copy of the federal estate tax return (Form 706 or 706-NA) to the Florida F-706 form.

- Mail the completed form and any necessary payment to: Florida Department of Revenue, PO Box 6460, Tallahassee, FL 32399-6460. Include a $5.00 fee if requesting a nontaxable certificate.

After the form is filed, it is reviewed by the Florida Department of Revenue. If further information is required or if adjustments are needed, they may reach out for additional details. Keep a copy of the form and all supporting documents for personal records and future reference.

Listed Questions and Answers

What is the Florida F-706 Form?

The Florida F-706 Form, also known as the Florida Estate Tax Return, is a document required for the estates of Florida residents, nonresidents, and nonresident aliens who owned property in Florida at the time of their death and are subject to federal estate tax filing requirements. The form calculates the estate tax due to the state of Florida based on allowable federal credits for state death taxes.

When is the Florida F-706 Form due?

The due date for filing the Florida F-706 and any payment due is within 9 months after the decedent's death, which aligns with the federal estate tax return deadline. If an extension is needed for filing or paying the tax, requests must be directed to the Internal Revenue Service (IRS), as Florida does not offer a separate extension form. The state will honor the same extension granted by the IRS but requires copies of the federal extension request and approval to be sent to the Florida Department of Revenue within 30 days of submitting or receiving them.

Are there penalties for late filing or payment of the Florida Estate Tax?

Yes, penalties apply if the estate tax or the filing of Form F-706 is delayed past its due date, including an initial late payment penalty of 10% of the unpaid tax. This penalty increases to 20% after 30 days. Further penalties for negligence or intentional disregard can add an additional 10% per month, up to a 50% maximum. In cases of fraud, a penalty of 100% of the tax due can be imposed. However, interest on late payments also accumulates from the original due date until the tax is paid in full.

How can someone amend a previously filed Florida F-706 Form?

If there is a need to amend an already filed Form F-706, one must complete a new form and check the box indicating it's an amended return. If amendments result from changes to the federal estate tax return, a detailed statement describing the reasons for the changes, alongside relevant documents, including any communications received from the IRS and the amended federal tax return itself, must be attached. This ensures accuracy and helps in re-evaluating the estate tax obligations to Florida.

Common mistakes

Not attaching a copy of the federal estate tax return (Form 706 or 706-NA) is a common mistake. The Florida F-706 requires this documentation for a complete submission.

Incorrectly calculating the estate tax due or overpayment to Florida can lead to processing delays or incorrect assessments. This often occurs in Part IV of the form, where individuals must accurately subtract and add relevant figures.

Failure to submit proof of payment for estate, inheritance, or other death taxes properly paid to other states, when applicable, can result in the denial of these deductions for Florida residents. This proof is crucial for ensuring that double taxation does not occur.

Forgetting to check the box for an amended return when filing a correction to a previously submitted F-706 leads to confusion and potentially incorrect processing by the Florida Department of Revenue.

Omitting the signature of the personal representative or the preparer other than the personal representative compromises the validity of the return. Both signatures are required under penalties of perjury to affirm the accuracy of the information provided.

Ignoring the need to request an extension for filing or paying the estate tax from the Internal Revenue Service (IRS) can result in penalties and interest. When granted an extension by the IRS, the Florida Department of Revenue also requires notification through submission of copies of the federal extension request and approval.

Documents used along the form

When dealing with estate affairs in Florida, particularly in preparing the F-706 Florida Estate Tax Return, several other forms and documents often come into use to ensure compliance and thoroughness in the estate settlement process. These forms play various roles from asserting tax liabilities to transferring assets and many are necessary for both legal and procedural reasons.

- IRS Form 706: This is the federal estate tax return and is required for estates that might owe federal estate tax. It is also used to calculate the state death tax credit.

- Florida Form DR-312: Also known as the Affidavit of No Florida Estate Tax Due, it's used when an estate does not meet the filing requirement for a formal estate tax return due to not owing any federal estate tax.

- Florida Form DR-313: Declaration of Domicile, utilized to establish Florida residency which can affect estate tax considerations.

- Last Will and Testament: This document outlines the decedent’s wishes regarding the distribution of their estate which is vital for estate processing.

- Death Certificate: A certified death certificate is often required to accompany various estate filings to confirm the decedent's date and place of death.

- Proof of Payment to Other States: If the estate paid inheritance or other death taxes to other states, these payments must be documented and filed with Florida if those taxes affect Florida estate taxes.

- Court Letters of Administration: These documents authorize the personal representative to act on behalf of the estate, including filing taxes.

- IRS Form 56: This form is filed with the IRS to notify them of the fiduciary relationship of the personal representative overseeing the estate.

- Schedule of Assets: Though not a formal form, a detailed list of the estate’s assets, including those located in Florida, is necessary for both the F-706 and federal Form 706.

- IRS Transfer Certificate: Required for nonresident alien estates, it shows that the IRS has consented to the transfer of property from the estate.

Accurate and timely filing of these documents helps in the seamless management of the decedent's estate, potentially easing the burden on the personal representative and the beneficiaries. It's crucial to understand the role each document plays and to ensure that they are correctly prepared and filed, adhering to both state and federal estate regulations.

Similar forms

The Florida F-706 form, used for reporting estate taxes to the Florida Department of Revenue, has similarities with other estate-related documents that are crucial in the administration of an estate following the death of an individual. These documents each serve distinct purposes but are interrelated in the process of settling an estate.

The Federal Form 706 is the most directly comparable document to the Florida F-706. This form, required by the Internal Revenue Service (IRS), is used to calculate estate tax at the federal level. Both the Federal Form 706 and the Florida F-706 derive the applicable estate taxes from the value of the decedent's estate. However, while the Federal Form 706 focuses on the overall estate's value and the corresponding federal taxes due, the Florida F-706 specifically calculates the state estate tax liability, crediting any applicable federal estate taxes and detailing taxes paid to other states.

Form 706-NA shares a purpose with the Florida F-706, but it is designated for nonresident aliens. This form is used when a nonresident alien decedent has assets in the United States, including Florida, and calculates the estate tax due on U.S.-situated assets. Like the Florida F-706, it takes into account the federal credit for state death taxes to determine the portion of estate tax attributable to Florida assets. The relationship between these forms underscores the importance of coordinated tax reporting between federal and state levels, especially in the context of international estate planning.

Florida Form DR-312, Affidavit of No Florida Estate Tax Due, while not a tax return, is related to the Florida F-706 in its function within estate settlement processes. It's used when a decedent's estate is not subject to Florida estate tax, hence not requiring the filing of a Florida F-706 form. This affidavit may be necessary to remove a Florida estate tax lien, allowing the estate to be settled and assets distributed without filing a full estate tax return. The connectivity between the DR-312 and F-706 forms highlights the varying requirements based on the size and tax liability of the estate in question.

Dos and Don'ts

When preparing to fill out the Florida F 706 form, there are essential steps and precautions that must be taken to ensure accuracy and compliance. Below is a guide comprising seven do's and don'ts to assist in this process.

Do's:

- Attach a signed copy of the federal Form 706 or 706-NA if the decedent's date of death is on or before December 31, 2004. This is crucial for all Florida residents, nonresidents, and nonresident aliens with Florida property who are required to file a federal estate tax return.

- File and pay within 9 months after the decedent’s death. Timeliness is key to avoiding penalties and ensures that the filing process aligns with both state and federal timelines.

- Apply for an extension through the IRS if more time is needed. Remember, Florida will recognize a federal extension, but formal notification to the Florida Department of Revenue is required.

- Pay any applicable taxes to other states if the decedent was a Florida resident and provide proof of such payments. This will ensure an accurate calculation of any Florida estate tax due or an overpayment.

- Include the personal representative’s signature and, if applicable, the preparer's. This verifies under penalties of perjury that the information provided is correct.

- Check the amended return box if submitting changes to an already filed return, especially if prompted by modifications to your federal Form 706 or 706-NA.

- Seek assistance if needed by utilizing the resources provided by the Florida Department of Revenue or contacting Taxpayer Services.

Don'ts:

- Do not disregard the specific filing requirements based on the decedent's date of death. Understanding whether Form F-706 needs to be filed is fundamental.

- Avoid filing late without securing an extension. Doing so can lead to unnecessary penalties and interest that could have been avoided.

- Do not forget to include the $5.00 fee if requesting a nontaxable certificate, as this is part of the submission requirements.

- Do not omit proof of death tax payments to other states for Florida residents. This proof is essential for the accurate calculation of the estate tax.

- Refrain from submitting incomplete forms. An incomplete form can lead to processing delays and potential penalties.

- Do not ignore the importance of the personal representative’s or the preparer’s signature. This is a certification of the return's accuracy.

- Avoid negligence in calculating taxes due or overpayments. Accurate calculations are critical to prevent the accrual of penalties and interest for underpayments.

By adhering to these guidelines, the process of completing and filing the Florida F 706 form can be smooth and compliant with state requirements.

Misconceptions

There are several common misconceptions about the Florida F-706 form, also known as the Florida Estate Tax Return, that individuals often encounter. Understanding these misconceptions can clarify the filing process and requirements. Below are eight misconceptions and their explanations:

The F-706 is required for all Florida decedents: Not true. The F-706 is only required for estates of decedents dying on or before December 31, 2004, that are also required to file a federal estate tax return (Form 706 or Form 706-NA). Estates of decedents dying after this date do not require an F-706 filing with the state of Florida.

Form F-706 functions as an estate tax for Florida residents only: Incorrect. The form is used for Florida residents, nonresidents, and nonresident aliens with Florida property. The distinction is crucial for determining the tax responsibilities for estates involving property within Florida.

You must file Form F-706 separately with the state of Florida if an extension is granted by the IRS: This is a misunderstanding. Florida will recognize the same extension granted by the IRS for filing and payment, but you must submit copies of the federal extension request and approval to the Florida Department of Revenue.

Amending an F-706 requires only a change to the original submission: Not correct. To amend an F-706, a new form must be filled out, checking the amended return box, and including a statement describing the reason for the amendment and any relevant documents, including amended federal returns if applicable.

Penalties are fixed and cannot be adjusted: Incorrect. The Florida Department of Revenue has the authority to compromise or settle penalties related to the late payment, negligence, or fraud, in accordance with state law.

Social Security Numbers (SSNs) are optional on Form F-706: This is false. SSNs are used as unique identifiers for tax administration and are required on the form. They are confidential and protected by law.

There is no penalty for late payment if the form is filed on time: Not true. Penalties apply for late payments even if the form is filed by the deadline. These penalties can increase over time and include interest on the unpaid tax.

A nontaxable certificate is automatically issued with Form F-706: Incorrect. A nontaxable certificate requests must be accompanied by a $5.00 fee, and is required separately if verifying that no Florida estate tax is due for the estate.

Clearing up these misconceptions ensures a smoother process for those handling estate affairs in Florida and aligns expectations with the legal requirements and state administration practices.

Key takeaways

The Florida F-706 form is a crucial document for the estate representatives of deceased individuals who were residents, nonresidents, or nonresident aliens with property in Florida. It outlines the procedure for calculating and paying estate taxes due to the state. Here are some key takeaways to understand:

- The requirement to file Form F-706 hinges on the decedent's date of death, with a clear demarcation: for deaths on or before December 31, 2004, the form is required; for deaths on or after January 1, 2005, it is not.

- For estates that must file, Form F-706 serves as the Florida Estate Tax Return and is necessary for those also required to file a federal estate tax return (Form 706 or Form 706-NA).

- A copy of the federal estate tax return must be attached to the Florida estate tax return upon submission.

- The form and any accompanying payment are due within 9 months of the decedent's death, coinciding with the federal estate tax return's due date.

- If an extension of time to file or pay is required, requests must be made through the Internal Revenue Service (IRS), as Florida follows the federal extension but requires notification and copies of federal documentation.

- Interest accrues on any unpaid Florida estate tax from the original due date until the tax is fully paid, emphasizing the importance of timely payments.

- For residents, estate taxes paid to other states can be submitted as proof to potentially lower the Florida estate tax burden. This includes the requisite final certificates of payment documenting specific amounts of tax, penalty, or interest paid.

- Amendments to a previously filed Form F-706 must be noted as such, with detailed explanations and documents related to any changes, especially those prompted by amendments to federal estate tax filings.

- Penalties and interest are imposed for late payments, with penalties varying based on the duration of the delay and the nature of the underpayment, such as negligence or fraud, while interest rates are updated semi-annually.

Moreover, the form functions under advisements related to the confidential handling of social security numbers, dictated by state and federal laws aimed at protecting individual privacy. Estate representatives must also navigate specific instructions regarding signatures — both of the personal representative and, if applicable, the preparer other than the personal representative.

Ultimately, the F-706 form encapsulates Florida's requirements for estate tax reporting and payment, offering a comprehensive outline for applicable estates to follow. It underscores the intertwining relationship between state and federal obligations, ensuring that estates with ties to Florida comply with local tax statutes while coordinating with broader federal mandates.

Popular PDF Documents

Florida Homeschool Requirements - Prepares parents for a successful homeschooling experience by guiding them through the initial legal requirements.

Healthcare Proxy Florida - Facilitate a smooth transition into our care with designated sections for both primary and secondary insurance information.

Radon Gas Florida - It explicitly states that incomplete applications will not be considered, emphasizing the importance of providing all requested details.