Fill Out a Valid Florida Sales Tax Template

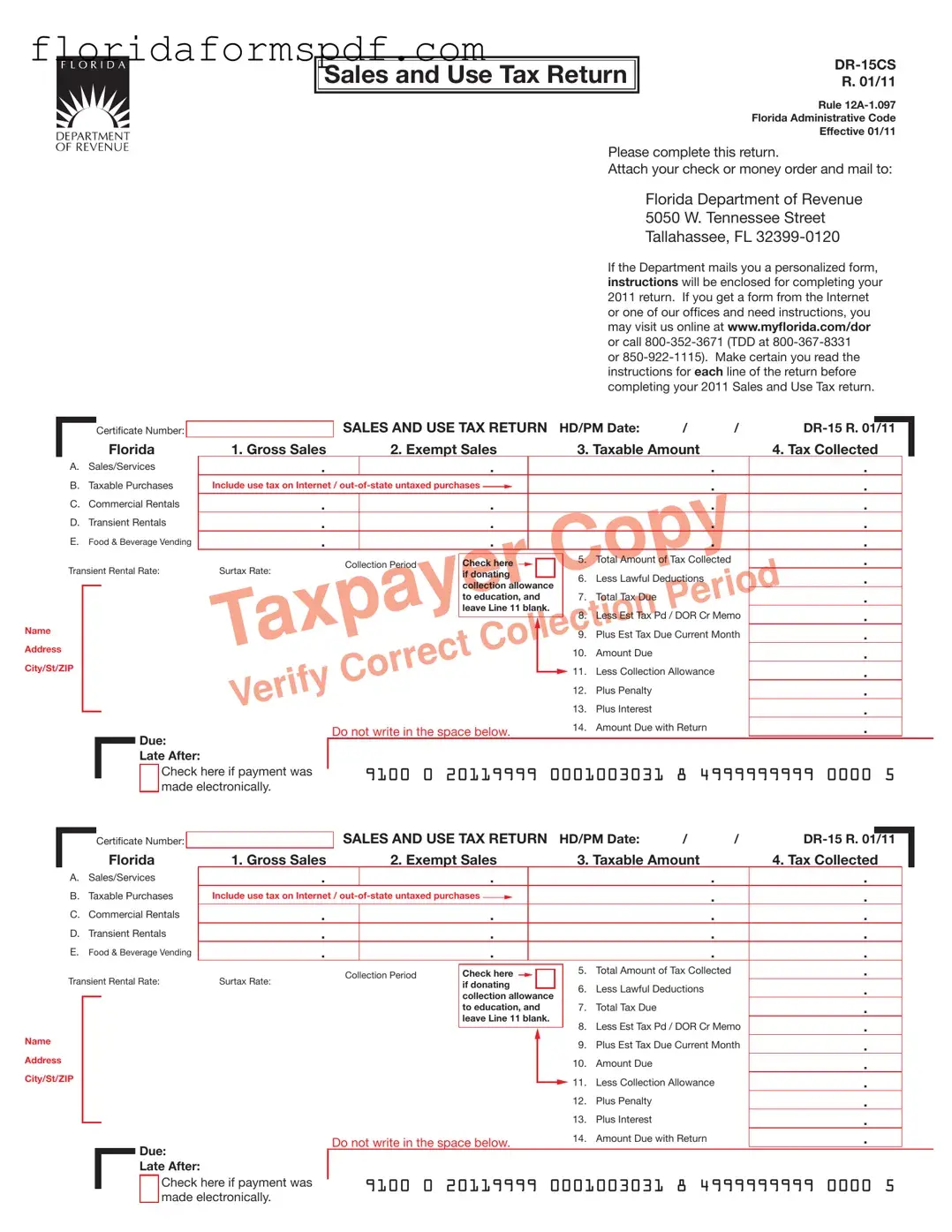

In navigating the intricacies of Florida's taxation system, businesses operating within the state are required to acquaint themselves with the Sales and Use Tax Return, formally known as DR-15CS. As delineated in the Florida Administrative Code, effective January 2011, the form plays a crucial role in the compliance and remittance of sales taxes to the Florida Department of Revenue. Located at 5050 W. Tennessee Street, Tallahassee, FL, the Department mandates that this form, complete with any applicable check or money order, be submitted to ensure adherence to state tax obligations. For those utilizing personalized forms sent by the Department, detailed instructions are typically enclosed, facilitating the proper completion of the 2011 return. Alternatively, the form is accessible via the Internet or at various offices, with further assistance available online at the official Department website or through direct contact via phone. The form meticulously outlines financial activities subject to taxation within the applicable period, including gross sales, exempt sales, and taxable amounts, alongside specific sections dedicated to sales/services, taxable purchases, commercial and transient rentals, and food and beverage vending. This structured approach aids in determining the total amount of tax collected, inclusive of additional elements like the transient rental rate and surtax rate, while also accounting for lawful deductions, estimated payments, and penalties, culminating in the accurate computation of total tax due. Significantly, the form also incorporates provisions for discretionary sales surtax, highlighting the nuanced application of county-specific rates on taxable transactions, underscoring the importance of accurate completion to ensure proper distribution of funds to local governments. The form presents an avenue for businesses to contribute towards educational initiatives through the designation of collection allowances, emphasizing the broader societal impact of compliance. With penalties established for fraudulent or negligent misrepresentation, signatories affirm the truthfulness of their submissions under the weight of perjury, ensuring accountability and integrity in the tax reporting process.

Document Preview Example

Sales and Use Tax Return

Sales and Use Tax Return

R. 01/11

Rule

Florida Administrative Code

Effective 01/11

Please complete this return.

Attach your check or money order and mail to:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Florida Department of Revenue |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5050 W. Tennessee Street |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tallahassee, FL |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If the Department mails you a personalized form, |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

instructions will be enclosed for completing your |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2011 return. If you get a form from the Internet |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

or one of our ofices and need instructions, you |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

may visit us online at www.mylorida.com/dor |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

or call |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

or |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

instructions for each line of the return before |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

completing your 2011 Sales and Use Tax return. |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

SALES AND USE TAX RETURN |

HD/PM Date: |

/ |

/ |

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

Certiicate Number: |

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

Florida |

1. Gross Sales |

|

|

2. Exempt Sales |

|

|

3. Taxable Amount |

|

4. Tax Collected |

|

|

||||||||||||||||

|

|

A. |

Sales/Services |

|

. |

|

|

|

. |

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||

|

|

B. |

Taxable Purchases |

|

Include use tax on Internet / |

|

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

C. |

Commercial Rentals |

|

. |

|

|

|

. |

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||

|

|

D. |

Transient Rentals |

|

. |

|

|

|

. |

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||

|

|

E. |

Food & Beverage Vending |

|

. |

|

|

|

. |

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Amount of Tax Collected |

|

. |

|

|

|

|

|||||||

|

|

Transient Rental Rate: |

Surtax Rate: |

|

Collection Period |

Check here |

|

|

|

|

|

5. |

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

if donating |

|

|

|

6. |

Less Lawful Deductions |

|

. |

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

collection allowance |

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

to education, and |

|

7. |

Total Tax Due |

|

|

. |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

leave Line 11 blank. |

|

|

|

|

|

|

|

|

|

|

|

||||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8. Less Est Tax Pd / DOR Cr Memo |

. |

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9. Plus Est Tax Due Current Month |

. |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10. |

Amount Due |

|

|

. |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

City/St/ZIP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11. |

Less Collection Allowance |

|

. |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12. |

Plus Penalty |

|

|

. |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13. |

Plus Interest |

|

|

. |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

Due: |

|

Do not write in the space below. |

14. |

Amount Due with Return |

|

. |

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

Late After: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

Check here if payment was |

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

9100 0 20119999 0001003031 8 4999999999 0000 5 |

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

made electronically. |

|

SALES AND USE TAX RETURN |

HD/PM Date: |

/ |

/ |

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

Certiicate Number: |

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

Florida |

1. Gross Sales |

|

|

2. Exempt Sales |

|

|

3. Taxable Amount |

|

4. Tax Collected |

|

|

||||||||||||||||

|

|

A. |

Sales/Services |

|

. |

|

|

|

. |

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||

|

|

B. |

Taxable Purchases |

|

Include use tax on Internet / |

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

C. |

Commercial Rentals |

|

. |

|

|

|

. |

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||

|

|

D. |

Transient Rentals |

|

. |

|

|

|

. |

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||

|

|

E. |

Food & Beverage Vending |

|

. |

|

|

|

. |

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Amount of Tax Collected |

|

. |

|

|

|

|

||||||||

|

|

Transient Rental Rate: |

Surtax Rate: |

|

Collection Period |

Check here |

|

|

|

|

5. |

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

if donating |

|

|

6. |

Less Lawful Deductions |

|

. |

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

collection allowance |

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

to education, and |

|

7. |

Total Tax Due |

|

|

. |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

leave Line 11 blank. |

|

|

|

|

|

|

|

|

|

|

|

||||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8. Less Est Tax Pd / DOR Cr Memo |

. |

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9. Plus Est Tax Due Current Month |

. |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10. |

Amount Due |

|

|

. |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

City/St/ZIP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11. |

Less Collection Allowance |

|

. |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12. |

Plus Penalty |

|

|

. |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13. |

Plus Interest |

|

|

. |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

Due: |

|

Do not write in the space below. |

14. |

Amount Due with Return |

|

. |

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

Late After: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

Check here if payment was |

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

9100 0 20119999 0001003031 8 4999999999 0000 5 |

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

made electronically. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Proper Collection of Tax: Florida’s general sales tax rate is 6 percent; however, there is an established “bracket system” for calculating the tax due when any part of each total taxable sale is less than a whole dollar amount. Other rates may also apply. See instructions.

Discretionary Sales Surtax: Most counties levy a discretionary sales surtax on most transactions subject to sales and use tax. These taxes are distributed to local governments throughout the state. The amount of money distributed is based on how you complete your tax return, especially the lines on the back of the return. Dealers should impose discretionary sales surtax on taxable sales when delivery or use occurs in a county that imposes surtax. Please see Form

Fraud Penalties: There are speciic penalties imposed for fraud, fraudulent claim of exemption, failure to collect and pay over, or an attempt to evade or defeat the sales tax. Please see the instructions for detailed information regarding the penalties, ines, and punishments for certain sales tax offenses.

Under penalties of perjury, I declare that I have read this return and the facts stated in it are true (sections 92.525(2), 212.12, and 837.06, Florida Statutes).

Signature of Taxpayer |

Date |

Signature of Preparer |

Date |

( ___________ ) ____________________________________________ |

|

( ___________ ) ____________________________________________ |

|

Telephone Number |

|

Telephone Number |

|

Discretionary Sales Surtax ( Lines 15(a) through 15(d) )

15(a). |

Exempt Amount of Items Over $5,000 (included in Column 3) |

15(a). _________________________________ |

15(b). |

Other Taxable Amounts NOT Subject to Surtax (included in Column 3) |

15(b). _________________________________ |

15(c). |

Amounts Subject to Surtax at a Rate Different Than Your County Surtax Rate (included in Column 3) |

15(c). _________________________________ |

15(d). |

Total Amount of Discretionary Sales Surtax Collected (included in Column 4) |

15(d). _________________________________ |

16. |

Total Enterprise Zone Jobs Credits (included in Line 6) |

16. _________________________________ |

17. |

Taxable Sales/Untaxed Purchases of Electric Power or Energy — 7% Rate (included in Line A) |

17. _________________________________ |

18. |

Taxable Sales/Untaxed Purchases of Dyed Diesel Fuel — 6% Rate (included in Line A) |

18. _________________________________ |

19. |

Taxable Sales from Amusement Machines (included in Line A) |

19. _________________________________ |

20. |

Rural and/or Urban High Crime Area Job Tax Credits |

20. _________________________________ |

21. |

Other Authorized Credits |

21. _________________________________ |

Under penalties of perjury, I declare that I have read this return and the facts stated in it are true (sections 92.525(2), 212.12, and 837.06, Florida Statutes).

Signature of Taxpayer |

Date |

Signature of Preparer |

Date |

( ___________ ) ____________________________________________ |

|

( ___________ ) ____________________________________________ |

|

Telephone Number |

|

Telephone Number |

|

Discretionary Sales Surtax ( Lines 15(a) through 15(d) )

15(a). |

Exempt Amount of Items Over $5,000 (included in Column 3) |

15(a). _________________________________ |

15(b). |

Other Taxable Amounts NOT Subject to Surtax (included in Column 3) |

15(b). _________________________________ |

15(c). |

Amounts Subject to Surtax at a Rate Different Than Your County Surtax Rate (included in Column 3) |

15(c). _________________________________ |

15(d). |

Total Amount of Discretionary Sales Surtax Collected (included in Column 4) |

15(d). _________________________________ |

16. |

Total Enterprise Zone Jobs Credits (included in Line 6) |

16. _________________________________ |

17. |

Taxable Sales/Untaxed Purchases of Electric Power or Energy — 7% Rate (included in Line A) |

17. _________________________________ |

18. |

Taxable Sales/Untaxed Purchases of Dyed Diesel Fuel — 6% Rate (included in Line A) |

18. _________________________________ |

19. |

Taxable Sales from Amusement Machines (included in Line A) |

19. _________________________________ |

20. |

Rural and/or Urban High Crime Area Job Tax Credits |

20. _________________________________ |

21. |

Other Authorized Credits |

21. _________________________________ |

Document Overview

| Fact Name | Description |

|---|---|

| Form Title | Sales and Use Tax Return DR-15CS |

| Form Revision Date | January 2011 (01/11) |

| Governing Rule | Rule 12A-1.097, Florida Administrative Code |

| Mailing Address | Florida Department of Revenue, 5050 W. Tennessee Street, Tallahassee, FL 32399-0120 |

| Assistance and Instructions | Available online at www.myflorida.com/dor or via phone at 800-352-3671 (TDD 800-367-8331 or 850-922-1115) |

| Document Purpose | For reporting Gross Sales, Exempt Sales, and Taxable Amounts; calculating and submitting Sales and Use Taxes due |

| Signature Requirement | Must be signed under penalties of perjury affirming the accuracy of information provided |

| Governing Laws | Sections 92.525(2), 212.12, and 837.06, Florida Statutes |

Instructions on How to Fill Out Florida Sales Tax

Filing a sales tax return in Florida is an essential task for many businesses, and it's important to approach this responsibility with accuracy and diligence. Every registered business must regularly complete and submit their sales and use tax returns to maintain compliance with Florida's tax laws. This form, known as Form DR-15CS, ensures that the appropriate taxes collected from customers are remitted to the state. It's not just about reporting the sales made but also about calculating the correct amount of tax, considering exempt sales, and applying any relevant deductions or surtaxes. For those filling out this form for the first time or needing a refresher, the process might seem complex, but breaking it down step by step can simplify it.

- Enter your business's name, address, city, state, and ZIP code in the designated areas at the top of the form.

- Fill in the date of the reporting period and your Certificate Number in the fields provided at the top of the form.

- Report your Gross Sales in the first line. This includes all sales before deductions.

- List out any Exempt Sales on the second line. These are sales not subject to sales tax under Florida law.

- Calculate the Taxable Amount by subtracting the exempt sales from the gross sales and enter this amount on the third line.

- Detail the amount of tax collected for various types of transactions in the appropriate sections including Sales/Services, Taxable Purchases, Commercial Rentals, Transient Rentals, and Food & Beverage Vending.

- Add up the total amount of tax collected from all types and indicate this in the Total Amount of Tax Collected section.

- If applicable, indicate any lawful deductions that can reduce the amount of tax due.

- Complete the section on the back regarding the discretionary sales surtax. This includes reporting the exempt amount of items over $5,000, other taxable amounts not subject to the surtax, amounts subject to surtax at a different rate, and the total discretionary sales surtax collected.

- Sign and date the return. If someone prepared the return on behalf of the business, that individual should also sign and date the form and provide their telephone number.

- Attach a check or money order for the amount due, considering any collection allowances, penalties, or interest, if applicable.

- Mail the completed form and payment to the Florida Department of Revenue at the address provided on the form.

Completing the Florida Sales and Use Tax Return accurately is crucial for any business to comply with state laws and avoid potential penalties. It's not only about paying what's due but also about understanding how different transactions are taxed, including the standard sales tax, discretionary surtax, and any exceptions. If there are any doubts or complications during the process, consulting the instructions provided by the Florida Department of Revenue or seeking professional advice can provide clarity and ensure that the form is filled out correctly.

Listed Questions and Answers

What is the Florida Sales and Use Tax Return?

The Florida Sales and Use Tax Return, form DR-15CS, is a document that businesses in Florida must complete and submit to report and pay the sales and use taxes collected from customers. This form details the amount of sales and services, exempt sales, taxable purchases, among other financial figures relevant to tax collection and remittance to the Florida Department of Revenue.

Where should the Florida Sales and Use Tax Return be sent?

Completed forms, along with the appropriate payment (if applicable), should be mailed to the Florida Department of Revenue at 5050 W. Tennessee Street, Tallahassee, FL 32399-0120.

Can I obtain and submit this form online?

Yes, the form can be obtained from the Florida Department of Revenue’s website at www.myflorida.com/dor. Taxpayers have the option to submit the form and payment electronically through the same website, which offers a convenient way to manage tax responsibilities.

What constitutes Gross Sales on this form?

Gross Sales refer to the total amount of sales and services before any deductions are made for exempt sales or lawful deductions. This figure represents the comprehensive revenue generated from taxable and nontaxable sales activities.

How are Exempt Sales handled?

Exempt Sales are sales that are not subject to tax under Florida law. These could include certain types of goods or services deemed nontaxable. It's crucial to document these correctly to ensure accurate tax reporting and compliance.

What is the significance of the Taxable Amount section?

The Taxable Amount section is where you deduct the sum of exempt sales from gross sales to determine the total amount of sales subject to sales tax. This figure is crucial for calculating the amount of tax due correctly.

How is the Total Tax Due calculated?

The Total Tax Due is calculated by subtracting lawful deductions and previously paid estimated taxes from the taxable amount, then adding any estimated tax due for the current period. This figure represents the total amount owed to the Department of Revenue for the collection period.

What are Lawful Deductions?

Lawful Deductions include any allowable deductions under Florida law, which might include returns, allowances, or any other deductions authorized by the Department of Revenue. These deductions are subtracted from the gross sales to arrive at the taxable sales figure.

What happens if the form is submitted late?

If the Sales and Use Tax Return is submitted after the due date, penalties and interest may be assessed on the unpaid tax amount. It is advisable to file and pay on time to avoid these additional charges.

What is the Discretionary Sales Surtax?

The Discretionary Sales Surtax is a county-imposed tax that applies to most transactions subject to the state sales and use tax. The rate varies by county. This surtax must be collected and remitted by businesses for taxable sales and services delivered within a county that imposes such a surtax. Information regarding specific county rates can be found on Form DR-15DSS or the Department of Revenue’s website.

Common mistakes

Filling out the Florida Sales Tax form, officially known as the DR-15CS, is a critical task for many businesses operating within the state. However, it's not uncommon for mistakes to be made in the process. Here are six common errors that can lead to complications or even fines.

- Not Reporting Exempt Sales Properly: It's crucial to accurately report exempt sales, which are sales not subject to sales tax. Many mistakenly blend these with taxable sales or fail to report them altogether.

- Incorrect Calculation of Taxable Amount: Determining the correct taxable amount can be tricky, especially with various exemptions and deductions. Errors here can lead to underpaying or overpaying taxes.

- Misunderstanding Use Tax on Out-of-State Purchases: Florida residents must pay a use tax on items purchased tax-free or untaxed from out-of-state. Not including these purchases as taxable purchases is a common oversight.

- Omitting Discretionary Sales Surtax: Many counties impose their own surtaxes. Failing to add these additional taxes when applicable can significantly affect the total tax due.

- Forgetting to Deduct the Collection Allowance: Florida allows for a collection allowance if the tax is paid timely. This deduction is often overlooked, leading businesses to overpay.

- Inaccurate Surtax Calculations: Not all transactions are subject to the same surtax rates, and some might be exempt up to certain amounts. Incorrect calculations here can lead to errors in the total amount of discretionary sales surtax collected and reported.

Aside from these specific mistakes, it's also essential to ensure that all information is complete and accurate, including business name, address, and certificate number. Attention to detail and a thorough understanding of Florida's tax laws can help make the tax filing process smoother and keep businesses compliant.

Documents used along the form

When preparing and filing the Florida Sales Tax Form, businesses often need additional documents and forms to accurately report and pay their taxes. These documents are crucial for maintaining compliance with Florida's tax laws and ensuring accurate tax reporting. Below is an overview of other forms and documents frequently used alongside the Florida Sales Sales and Use Tax Return (DR-15).

- DR-15DSS (Discretionary Sales Surtax Information): This provides information on county-specific discretionary sales surtax rates, which must be applied to sales when the delivery or use occurs in a county that imposes such a surtax.

- Annual Resale Certificate for Sales Tax (DR-13): Issued by the Florida Department of Revenue, this certificate allows businesses to make tax-exempt purchases of goods that will be resold or rented.

- Florida Business Tax Application (DR-1): For new businesses, this form is required to register for a sales and use tax permit in Florida.

- Sales and Use Tax Exemption Certificate (DR-14): Businesses use this to document tax-exempt transactions, such as sales to nonprofit organizations.

- Use Tax Return (DR-15MO): For out-of-state purchases where sales tax wasn't collected at the point of sale, businesses report and pay use tax through this form.

- Consumer’s Certificate of Exemption (DR-14): This certifies that an entity or organization is exempt from Florida sales tax.

- Solid Waste and Surcharge Return (DR-15SW): Certain businesses must file this form to report and pay the solid waste surcharge and fees.

- Transient Rental Tax Return (DR-15T): If renting living, sleeping, or housekeeping accommodations for periods six months or less, this return is used to report and pay taxes collected.

- Commercial Rental Tax Return (DR-15C): This applies to businesses engaged in the rental, lease, or license to use commercial real property in Florida.

Each form serves a specific purpose related to the regulation of sales and use tax in Florida. Understanding when and how to use these documents ensures businesses can successfully navigate their tax responsibilities, remain compliant, and avoid legal pitfalls. For detailed information and assistance, the Florida Department of Revenue's website and helpline provide valuable resources.

Similar forms

The Florida Sales Tax form is similar to several other types of legal and financial documents in its structure and purpose. This form, designed for reporting and paying sales and use taxes to the state, has counterparts at both state and federal levels, used for various tax reporting requirements. Below are a couple of documents that share similarities with the Florida Sales Tax form:

Federal IRS Form 941, Employer's Quarterly Federal Tax Return: Like the Florida Sales Tax form, IRS Form 941 is used by employers to report income taxes, social security tax, or Medicare tax withheld from employees' paychecks. Both forms are periodic and mandatory for compliance with tax laws. They require detailed financial calculations and include sections for calculating taxes due, adjustments, and any credits owed to the filer. The specificity of information, structured fields for calculations, and the purpose of maintaining tax compliance are common threads between these documents.

State Unemployment Tax Forms: Each state has its own version of a form for reporting unemployment taxes, similar to the Florida Sales Tax form in terms of state-level tax compliance. These forms typically require employers to report wages paid to employees and calculate the amount of unemployment tax due based on state-specific rates. Like the Florida Sales Tax form, they feature a combination of fixed and variable fields, tailored to the unique requirements of the respective tax. Both sets of forms play a crucial role in funding state-administered programs and services, necessitating accurate and timely filings to avoid penalties.

Understanding the different forms and their purposes helps ensure compliance with the myriad of tax obligations businesses face. While each form serves a specific tax-related function, their common goal is to facilitate the accurate collection and reporting of taxes to support governmental operations and services.

Dos and Don'ts

When filling out the Florida Sales Tax form, there are specific practices to follow for accuracy and compliance. Paying close attention to these guidelines can ensure that the process is smooth and error-free.

Do:

- Thoroughly read the instructions provided with your personalized form or online at the Florida Department of Revenue's website.

- Accurately calculate your total gross sales, including all taxable and exempt sales, before filling in the form.

- Apply the correct tax rate, including both the general sales tax and any applicable discretionary sales surtax based on the delivery or use location.

- Report and include use tax on internet and out-of-state untaxed purchases, as required.

- Check the correct boxes for specific allowances or credits, such as education donations or enterprise zone jobs credits, if applicable.

- Sign and date the form, affirming under penalties of perjury that the information provided is accurate and true.

Don't:

- Omit any required sections or fail to attach a check or money order for the amount due. Incomplete submissions can lead to processing delays.

- Estimate figures or guess any amounts. Use exact figures for gross sales, exempt sales, taxable amounts, and tax collected to ensure accuracy.

- Ignore the discretionary sales surtax rates. Always check for the most current rates and apply them correctly based on the transaction location.

- Forget to calculate penalties or interest due if your return is late. These additional charges are mandatory and failure to include them could result in further penalties.

- Overlook the back of the return for specific discretionary sales surtax information or other applicable credits that could affect your total due.

- Submit the form without reviewing all entries. Even a minor mistake can have significant consequences, including potential audits or penalties.

Misconceptions

When it comes to filling out the Florida Sales Tax form, there are several misconceptions that can create confusion. Understanding these common mistakes can help ensure accuracy and compliance. Here’s a list of 10 misconceptions and the truth behind each one.

All sales are taxable. Not all sales in Florida are subject to sales tax. There are various exemptions such as certain grocery items and prescription medications.

Filing is only necessary if tax is owed. Even if no tax is due, businesses are required to file a return, reflecting their sales and any exempt transactions.

Only physical goods are taxable. Florida taxes many services as well, including but not limited to commercial rentals and certain services associated with personal property.

Internet and out-of-state purchases are not taxed. Florida requires businesses and individuals to pay use tax on items purchased tax-free from out-of-state vendors for use in Florida.

The statewide sales tax rate is all that applies. Most Florida counties have a discretionary sales surtax that applies to most transactions subject to the state sales tax.

Sales tax and use tax are the same. While they are similar, sales tax is imposed on sales within the state, and use tax applies to the use, consumption, distribution, or storage of goods in Florida when sales tax isn’t paid.

All counties have the same surtax rate. Discretionary sales surtax rates vary by county, impacting the total tax rate applicable to transactions in different areas.

Collection allowance is automatic. To benefit from the collection allowance, businesses must file timely and pay the tax due. This is not automatically deducted from the amount owed.

Electronic payment changes everything. Electing to pay electronically does change the method of submission, but it doesn’t alter filing requirements or due dates.

Penalties are not a concern for minor mistakes. Even minor inaccuracies can result in penalties and interest. It’s essential to fill out the form accurately and completely.

Ensuring an accurate understanding of the Florida Sales Tax form can save businesses time and protect them from unintended non-compliance penalties. Being aware of these misconceptions is a step in the right direction for any business operating in Florida.

Key takeaways

Filling out and using the Florida Sales Tax form, officially known as DR-15CS, is a crucial process for businesses to comply with state tax regulations. Understanding how to accurately complete this form ensures that businesses not only adhere to the law but also capitalize on potential benefits. Here are key takeaways to keep in mind:

- Understand the Taxable Amounts: It's essential to have a clear distinction between gross sales and taxable sales. Gross sales include the total of all sales transactions, whereas taxable sales are those subject to sales tax after exemptions have been applied. Careful calculation of these figures is paramount to avoid underpayment or overpayment of taxes.

- Exemptions and Deductions: Make sure to accurately report exempt sales and lawful deductions. These could range from certain types of goods and services that are not subject to sales tax, to specific items allowed by the Florida Department of Revenue. Incorrect reporting could lead to penalties or missed savings.

- Discretionary Sales Surtax: Florida allows counties to impose additional sales surtaxes. The rate varies by county, and it's crucial to apply the correct rate based on the location of the product delivery or service provision. This ensures compliance and accurate tax collection, benefiting local governments and communities.

- Penalties for Incorrect Reporting: The Florida Department of Revenue imposes strict penalties for fraud, failure to collect or remit sales tax, or attempts to evade taxes. It is imperative to maintain honesty and accuracy when filling out the form to avoid severe consequences, including fines and legal actions.

- Electronic Filing and Payment: If payment is made electronically, it should be indicated on the form. Utilizing electronic methods for filing and payment can streamline the process, ensuring timely and secure transactions with the Department of Revenue.

In summary, the accurate completion and submission of the Florida Sales Tax form require attention to detail and an understanding of taxable transactions, exemptions, and additional surtaxes. Businesses should stay informed of the latest tax codes and rates, maintain accurate sales records, and seek professional advice if necessary, to ensure full compliance with state tax laws.

Popular PDF Documents

Florida Hvac Efficiency Card - Promotes the installation of energy-efficient air conditioning systems through meticulous documentation of technical specifications.

Florida - Details the specific requirements for reporting employee names and social security numbers on the form.

Healthcare Proxy Florida - Access ease of use with clear instructions for both digital and physical submission of the patient intake form and supporting documents.