Free Loan Agreement Template for Florida

Entering into a financial agreement, especially in the vibrant economic landscape of Florida, requires a certain level of precision and understanding. The Florida Loan Agreement form serves as a crucial tool in this process, ensuring that both lenders and borrowers are on the same page regarding the terms of a loan. This formal document outlines the specifics of the loan, including the amount being borrowed, the repayment schedule, interest rates, and any collateral involved. Moreover, it delves into the responsibilities of each party, protecting their interests and providing a legal foundation should disputes arise. Intended to mitigate potential misunderstandings and legal conflicts, this agreement stands as a testament to the importance of clarity and mutual agreement in financial transactions. By clearly setting the expectations and obligations for both parties, the Florida Loan Agreement form not only facilitates smoother financial dealings but also contributes to the overall stability and trust in the financial market within the Sunshine State.

Document Preview Example

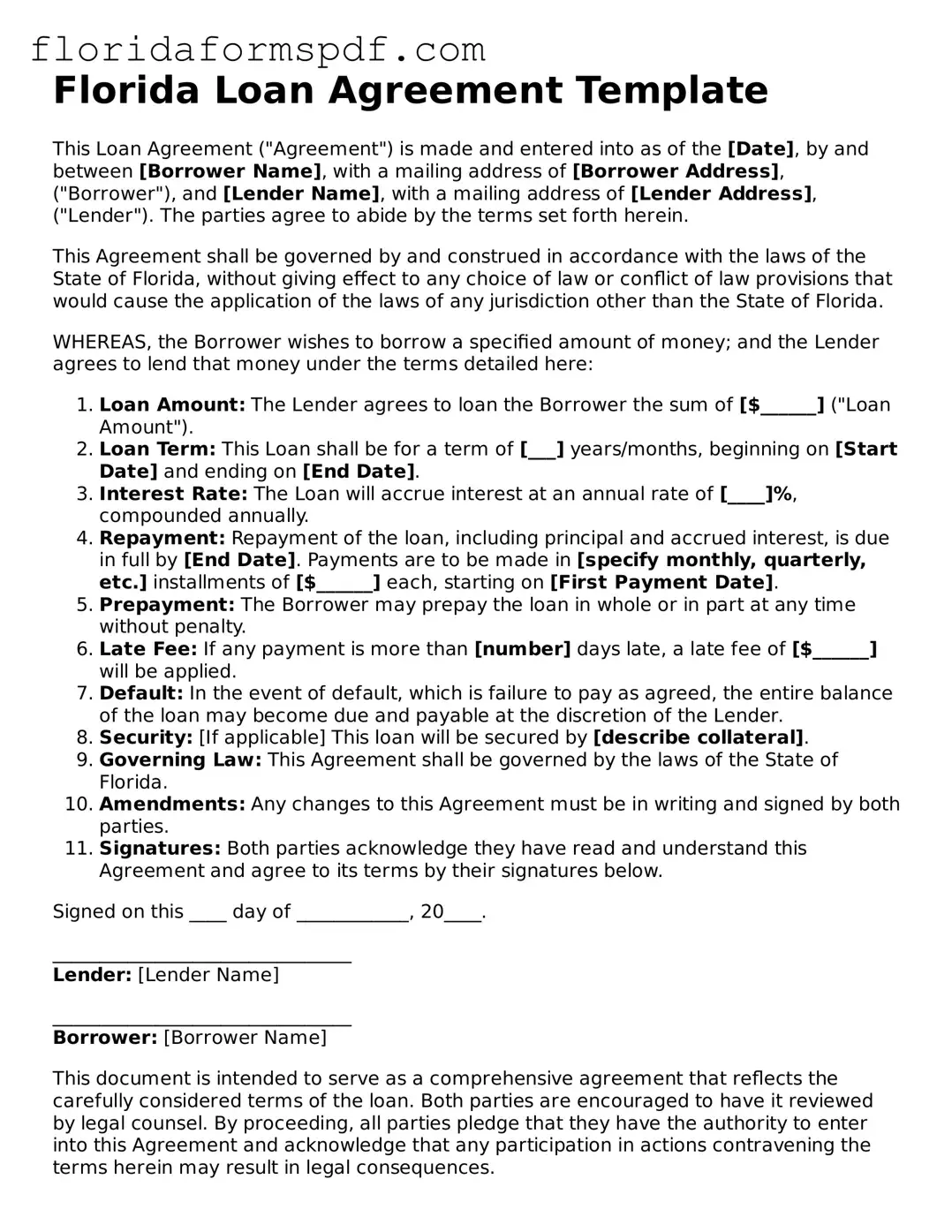

Florida Loan Agreement Template

This Loan Agreement ("Agreement") is made and entered into as of the [Date], by and between [Borrower Name], with a mailing address of [Borrower Address], ("Borrower"), and [Lender Name], with a mailing address of [Lender Address], ("Lender"). The parties agree to abide by the terms set forth herein.

This Agreement shall be governed by and construed in accordance with the laws of the State of Florida, without giving effect to any choice of law or conflict of law provisions that would cause the application of the laws of any jurisdiction other than the State of Florida.

WHEREAS, the Borrower wishes to borrow a specified amount of money; and the Lender agrees to lend that money under the terms detailed here:

- Loan Amount: The Lender agrees to loan the Borrower the sum of [$______] ("Loan Amount").

- Loan Term: This Loan shall be for a term of [___] years/months, beginning on [Start Date] and ending on [End Date].

- Interest Rate: The Loan will accrue interest at an annual rate of [____]%, compounded annually.

- Repayment: Repayment of the loan, including principal and accrued interest, is due in full by [End Date]. Payments are to be made in [specify monthly, quarterly, etc.] installments of [$______] each, starting on [First Payment Date].

- Prepayment: The Borrower may prepay the loan in whole or in part at any time without penalty.

- Late Fee: If any payment is more than [number] days late, a late fee of [$______] will be applied.

- Default: In the event of default, which is failure to pay as agreed, the entire balance of the loan may become due and payable at the discretion of the Lender.

- Security: [If applicable] This loan will be secured by [describe collateral].

- Governing Law: This Agreement shall be governed by the laws of the State of Florida.

- Amendments: Any changes to this Agreement must be in writing and signed by both parties.

- Signatures: Both parties acknowledge they have read and understand this Agreement and agree to its terms by their signatures below.

Signed on this ____ day of ____________, 20____.

________________________________

Lender: [Lender Name]

________________________________

Borrower: [Borrower Name]

This document is intended to serve as a comprehensive agreement that reflects the carefully considered terms of the loan. Both parties are encouraged to have it reviewed by legal counsel. By proceeding, all parties pledge that they have the authority to enter into this Agreement and acknowledge that any participation in actions contravening the terms herein may result in legal consequences.

PDF Characteristics

| Fact | Description |

|---|---|

| 1. Purpose | The Florida Loan Agreement form is used to outline the terms and conditions under which a loan will be provided. This includes the loan amount, interest rate, repayment schedule, and any collateral securing the loan. |

| 2. Governing Law | The agreement is governed by the laws of the State of Florida, ensuring any disputes regarding the agreement will be resolved under Florida's legal jurisdiction. |

| 3. Parties Involved | Typically involves two parties: the lender, who provides the loan, and the borrower, who receives the loan and agrees to repay it under the terms specified in the agreement. |

| 4. Documentation | Proper documentation through this form provides legal protection for both lender and borrower by clearly defining the loan's obligations and expectations. |

| 5. Collateral Security | Collateral may be required as security for the loan, which is specified within the agreement. If the borrower fails to repay, the lender has the right to seize the collateral as repayment. |

| 6. Interest and Repayment | The agreement details the interest rate applied to the borrowed sum and how and when the borrower is to repay the loan, which might include monthly payments over a specified period. |

| 7. Default Consequences | Outlines the consequences should the borrower fail to comply with the terms, such as late fees, legal actions, and the potential seizure of collateral. |

Instructions on How to Fill Out Florida Loan Agreement

After you've decided to draft a loan agreement in Florida, it's essential to understand the necessary steps to ensure the form is filled out correctly. A well-drafted loan agreement not only provides legal protection but also clarifies the obligations of each party. Whether it's a loan between friends or a more formal business arrangement, having a solid agreement in place can help prevent misunderstandings and disputes down the line.

- Gather all required information, including the full names and addresses of both the lender and the borrower, as well as any co-signers.

- Determine the loan amount. Write down the total amount of money that is being loaned in both words and numbers to ensure clarity.

- Agree upon the interest rate. If the loan will include interest, specify the rate. Remember, Florida might have laws dictating maximum allowable interest rates, so be sure to check the current regulations.

- Outline the repayment schedule. Detail how often payments will be made (e.g., monthly, quarterly) and specify if there is a final lump sum payment, often referred to as a "balloon payment."

- Specify the loan's purpose. Although not always necessary, detailing what the loan will be used for can help in understanding the terms.

- Include clauses on late payments and default. Clearly state any fees for late payments and the conditions under which the loan would be considered in default.

- State the governing law. Indicate that the agreement will be governed by the laws of the State of Florida.

- Decide if collateral will secure the loan. If the loan is to be secured with collateral, describe the collateral in detail in the agreement.

- Signatures. Ensure both the lender and the borrower sign the agreement in front of a notary. It's also a good idea to have witnesses sign, though this may not be legally required.

Once the loan agreement is fully executed, each party should keep a copy for their records. A properly filled out form will establish the legal obligations of the parties involved and provide a clear path forward in the lending process. Following the outlined steps can significantly reduce potential conflicts and help maintain positive relationships between the lender and borrower.

Listed Questions and Answers

What exactly is a Florida Loan Agreement form?

A Florida Loan Agreement form is a legally binding document between two parties, where one, the lender, agrees to loan a specific amount of money to the other, the borrower. This form outlines the terms and conditions of the loan, such as the interest rate, repayment schedule, and any collateral involved. It's specific to the state of Florida, ensuring it complies with local laws and regulations.

Who should use a Florida Loan Agreement form?

Individuals or businesses in Florida looking to lend or borrow money should use this form. It's suitable for a range of financial transactions, from personal loans between family members to more formal business investments. Having a written agreement in place protects both parties by clearly defining the terms of the loan.

Is a witness or notarization required for a Loan Agreement in Florida?

While Florida law doesn't mandatory require a witness or notarization for a Loan Agreement to be legally valid, having the document notarized or witnessed can add an extra layer of protection and authenticity. This step can be particularly beneficial in case of disputes or if proof of the agreement's validity and the parties' acknowledgment is required in a court of law.

What happens if a borrower fails to repay the loan as agreed?

If a borrower fails to repay the loan according to the terms set out in the agreement, the lender has the right to pursue legal action to recover the owed money. Depending on the agreement's provisions, this could involve claiming the collateral detailed in the loan agreement or filing a lawsuit to obtain a judgment against the borrower for the outstanding amount plus any applicable interest and fees.

Can the terms of a Florida Loan Agreement be modified?

Yes, the terms of a Florida Loan Agreement can be modified, but any changes must be agreed upon by both the lender and the borrower. It's best practice to document any amendments in writing and have both parties sign the updated agreement. This ensures that the modifications are legally binding and protect both parties' interests.

Are there any specific clauses that should be included in a Florida Loan Agreement?

Certain clauses are essential for protecting both the lender and the borrower, such as the loan amount, interest rate, repayment schedule, default and remedy provisions, and any collateral securing the loan. Including a Governing Law clause specifying that the agreement is subject to Florida state laws can also be beneficial for clarity and enforcement purposes.

How can I ensure that my Florida Loan Agreement is legally binding?

To ensure your Florida Loan Agreement is legally binding, make sure it includes all critical terms and conditions, is signed by both the lender and the borrower, and complies with Florida state laws and regulations. Consultation with a legal professional can provide additional assurance that your agreement is valid and enforceable.

What is the difference between a secured and an unsecured Loan Agreement?

A secured Loan Agreement involves the borrower pledging an asset as collateral for the loan, which the lender can claim if the borrower defaults on the loan. An unsecured Loan Agreement does not involve collateral. Therefore, the lender assumes a higher risk since there is no specific asset to claim in case of default. Secured loans typically offer lower interest rates than unsecured loans due to this reduced risk.

Can a Florida Loan Agreement be canceled?

A Florida Loan Agreement can be canceled if both the lender and the borrower agree to terminate it in writing. Conditions for cancellation or early repayment terms should ideally be detailed in the original agreement to simplify the process. However, depending on the terms of the agreement, canceling it may involve penalties or fees.

This FAQ section should provide a comprehensive overview for individuals looking to understand more about Florida Loan Agreements, whether they are lending or borrowing money in the state of Florida.Common mistakes

When individuals fill out the Florida Loan Agreement form, several common mistakes can lead to potential issues or misunderstandings down the line. It's important to approach this document with care and attention to detail to ensure all terms are clear and legally binding. Below are five mistakes often made during this process:

Not including the full legal names of all parties involved. Sometimes, people use nicknames or incomplete names, which can create ambiguities about the identities of the lender and borrower.

Failing to specify the loan amount in clear terms. It's crucial to write out the loan amount in both words and numbers to prevent any confusion about the total sum being lent.

Omitting the repayment schedule. The agreement should clearly state the due dates or timeline for repayments, including any grace periods or late fees.

Skipping the interest rate details. If the loan includes interest, the exact rate and how it's calculated should be specified. Without this, disagreements may arise over accrued interest.

Not signing the document. An often-overlooked but fundamental error is the failure to have the document signed by all parties. Legal documents require signatures for enforcement and validity.

Avoiding these mistakes will lead to a clearer, more enforceable agreement. It's also wise to consider seeking professional advice to ensure that the document fully protects your interests and complies with Florida state laws.

Documents used along the form

When entering into a loan agreement in Florida, several documents often accompany the primary contract to ensure a smooth, legally binding, and well-documented transaction. These documents help protect both the lender and the borrower by clarifying the terms, outlining the responsibilities of each party, and providing legal proofs and assurances. Here is a concise description of ten such ancillary documents that are typically utilized alongside the Florida Loan Agreement form:

- Promissory Note: A written promise by the borrower to pay a specified sum of money to the lender by a certain date. It outlines the repayment structure, including interest rates and payment schedules.

- Mortgage or Deed of Trust: These documents secure the loan by using the borrower's property as collateral. If the borrower fails to repay the loan, these documents provide the legal framework for the lender to foreclose on the property.

- Guaranty: A guaranty is a promise made by a third party to assume the repayment responsibility if the borrower defaults. This adds an extra layer of security for the lender.

- Disclosure Statements: Required by federal and state law, these statements provide the borrower with detailed information about the loan's costs and terms.

- Insurance Policies: Borrowers are often required to maintain insurance policies, such as property insurance, which protects the collateral from damage, and, in some cases, life insurance on the borrower to secure the repayment of the loan in case of their death.

- Title Documents: These documents verify the legal ownership of the property being used as collateral and ensure that the property is free of any other claims or liens.

- Amortization Schedule: This is a table detailing each payment on the loan over time, breaking down the amounts going toward the principal and interest.

- UCC-1 Financing Statement: For loans involving personal property (as opposed to real property) as collateral, a UCC-1 filing may be required to publicly declare the lender's interest in the borrower's personal property.

- Compliance Agreement: This document ensures that the borrower agrees to comply with all relevant laws and regulations affecting the property or the loan transaction.

- Environmental Indemnity Agreement: If the collateral involves real estate, this document protects the lender from liability for environmental contamination issues that might arise on the property.

Together, these documents form a comprehensive framework that supports the loan agreement, detailing the obligations and rights of both parties involved in the lending transaction. They play a critical role in managing risk and ensuring that both lenders and borrowers are informed and protected throughout the duration of the loan.

Similar forms

The Florida Loan Agreement form is similar to several other types of financial documents, although it serves a specific purpose within the context of borrowing and lending money. This form delineates the terms and conditions under which money is lent, setting clear expectations for both the borrower and the lender. The details include the loan amount, interest rate, repayment schedule, and any collateral required. Understanding the similarities to other documents can provide a broader context to its functions and purpose.

The first document it bears resemblance to is the Personal Loan Agreement. This document is typically used between individuals rather than institutions, and like the Florida Loan Agreement form, it outlines the loan's terms, including repayment schedule, interest rate, and any other conditions agreed upon by the parties involved. The primary similarity lies in the function of establishing a legally binding agreement between parties, ensuring the borrower's commitment to repay the loan under the specified terms.

Another similar document is the Promissory Note. A promissory note is essentially a written promise to pay a specific amount of money to a person or entity under agreed-upon terms. While it also contains details about the loan amount, interest rate, and repayment plan, it usually is less comprehensive and detailed than the Florida Loan Agreement form. The similarity lies in their shared goal of documenting the obligation to repay borrowed money, yet the loan agreement often includes more detailed provisions regarding the recourse in case of default.

The Mortgage Agreement shares some characteristics as well, particularly in regards to loans involving real property. Like the Florida Loan Agreement form, a mortgage agreement outlines the terms under which the mortgage lender provides funds to the borrower for purchasing property. The document serves as a lien on the property until the mortgage is fully repaid. The key difference is that while a mortgage agreement is secured by the property being purchased, a loan agreement might be secured by different types of collateral or be unsecured, depending on the terms agreed upon.

Lastly, the Line of Credit Agreement is also akin to the Florida Loan Drive In form. This document governs the terms of a line of credit offered by a lender to a borrower and outlines the maximum loan amount, the time frame during which the borrower can draw funds from the line of credit, and the repayment conditions. While the structure of this agreement differs by focusing on a revolving access to funds rather than a lump-sum loan, it similarly provides detailed terms on how the borrowed funds are to be repaid.

Dos and Don'ts

When it comes to filling out a Florida Loan Agreement form, accuracy and attention to detail are paramount. Such documents are legally binding and must reflect the terms of the loan clearly and correctly. Below are essential dos and don'ts to keep in mind.

Do:

- Review the entire form before starting to fill it out to ensure you understand all requirements and have all necessary information at hand.

- Use clear, legible handwriting if filling out the form by hand, or a readable font if filling it out electronically. This prevents misunderstandings or illegibility issues.

- Verify all the details, especially the names of the parties involved, the loan amount, the interest rate, repayment schedule, and any collateral involved. Mistakes in these details can lead to disputes or legal challenges.

- Keep a copy of the completed form for your records. This will be important for both parties if any disagreements arise or for personal record-keeping purposes.

Don't:

- Rush through the form without checking for errors. Taking your time can prevent costly mistakes.

- Leave any fields blank. If a section does not apply, write “N/A” (not applicable) instead of leaving it empty. Blank spaces can lead to uncertainty or fraudulent alterations.

- Forget to get the agreement signed by all parties. An unsigned agreement may not be enforceable.

- Ignore state-specific laws and regulations. The state of Florida may have unique requirements for loan agreements, and failing to comply with these can invalidate the contract.

Misconceptions

Many individuals in Florida, seeking to formalize loan arrangements, hold various misconceptions about the Loan Agreement form. These misunderstandings can lead to potential pitfalls. Shedding light on these can guide both lenders and borrowers through the process more effectively.

One Form Fits All: People often think that a single Loan Agreement form can suit any type of loan in Florida. In reality, different loans such as personal, business, or real estate loans may require specific provisions and considerations unique to their nature.

Legal Representation Isn’t Necessary: Some believe that they don’t need a lawyer to draft or review their Loan Agreement form. However, consulting a legal professional can ensure that the agreement complies with Florida’s laws and protects both parties’ interests.

Oral Agreements Suffice: While Florida law does recognize oral contracts under certain conditions, relying on an oral agreement for a loan can be risky and problematic for enforcement. A written Loan Agreement provides clear terms and conditions that are legally binding and enforceable.

No Need for Witnesses or Notarization: Many people assume that having witnesses or notarizing the document isn't necessary. Although not always legally required, these steps add a layer of verification and can be crucial for upholding the document in disputes.

Interest Rates Can Be Set Freely: Another common misconception is that parties can agree on any interest rate. However, Florida's usury laws impose limits on interest rates, exceeding which can render a loan agreement void and expose lenders to legal penalties.

A Loan Agreement Is Only About Payment Terms: While payment terms are crucial, a comprehensive Loan Agreement also addresses other important issues like default conditions, dispute resolution methods, and collateral requirements, making it multifaceted.

Signing Guarantees Loan Repayment: Even with a signed agreement, the guarantee of loan repayment is not absolute. Lenders may still face challenges in collection, and additional measures like securing collateral may be necessary for protection.

Templates Offer Complete Protection: Using a template might seem sufficient, but generic forms may not cover all specifics of the loan or comply with Florida law. Tailoring the agreement to the particular loan’s characteristics and legal requirements is advisable.

Any Amendments Require a New Agreement: It's often thought that changes to the loan terms necessitate drafting a new agreement. In fact, amendments can typically be made through written modifications or addenda, as long as both parties agree and endorse the changes.

Understanding these misconceptions and recognizing the importance of a well-constructed Loan Agreement can significantly affect the legal and financial health of the arrangement. It emphasizes the need for diligence and expert guidance when entering into any lending agreement in Florida.

Key takeaways

When filling out and using the Florida Loan Agreement form, it is important to understand its key aspects for the process to be smooth and compliant. Here are the takeaways to keep in mind:

- Ensure all parties' information is complete and accurate, including full names, addresses, and contact details. This ensures clear identification of the borrower and lender.

- Clearly state the loan amount and the terms of repayment, including the interest rate, payment schedule, and any late fees. Specifics prevent misunderstandacies and ensure both parties are on the same page.

- Include the purpose of the loan to define how the borrowed funds can be used. This helps in ensuring the loan is used for its intended purpose.

- Detail the consequences of a default, outlining the steps the lender can take if the borrower fails to meet the repayment terms. Clarity on this front protects the lender's interests.

- Have a clause regarding amendment and waiver, specifying how changes to the agreement can be made. This ensures that any modifications are mutually agreed upon and documented.

- Ensure the agreement is governed by Florida state law, emphasizing that any disputes will be resolved under the jurisdiction of Florida courts. This localizes the legal framework that will govern the agreement.

By paying attention to these details, parties involved can create a solid and enforceable loan agreement that aligns with Florida state regulations, safeguarding the interests of both the borrower and the lender.

Popular Florida Templates

30 Day Eviction Notice Florida - Understanding the implications and proper use of a Notice to Quit is essential for both landlords and tenants to navigate rental disputes.

Do You Need a Bill of Sale to Register a Car in Florida - This document can assist in resolving issues if there are later claims the motorcycle was stolen or involved in legal discrepancies.