Free Promissory Note Template for Florida

In the state of Florida, individuals and entities frequently rely on a financial instrument known as a promissory note to set the terms for borrowing money. This legal document is pivotal in clearly outlining the loan's key aspects, such as the amount borrowed, interest rate, repayment schedule, and the consequences of failing to meet the agreed-upon terms. Essential for both the lender and the borrower, the form serves as a formal commitment to ensure that the borrower repays the loan under the defined conditions. Moreover, the flexibility of the promissory note allows it to be tailored to fit a wide array of financing situations, from personal loans between family members to more complex transactions involving business financing. By adhering to the particulars stipulated in the Florida Promissory Note form, parties can safeguard their interests, promote clarity, and prevent potential disputes, making it a cornerstone of private lending practices within the state.

Document Preview Example

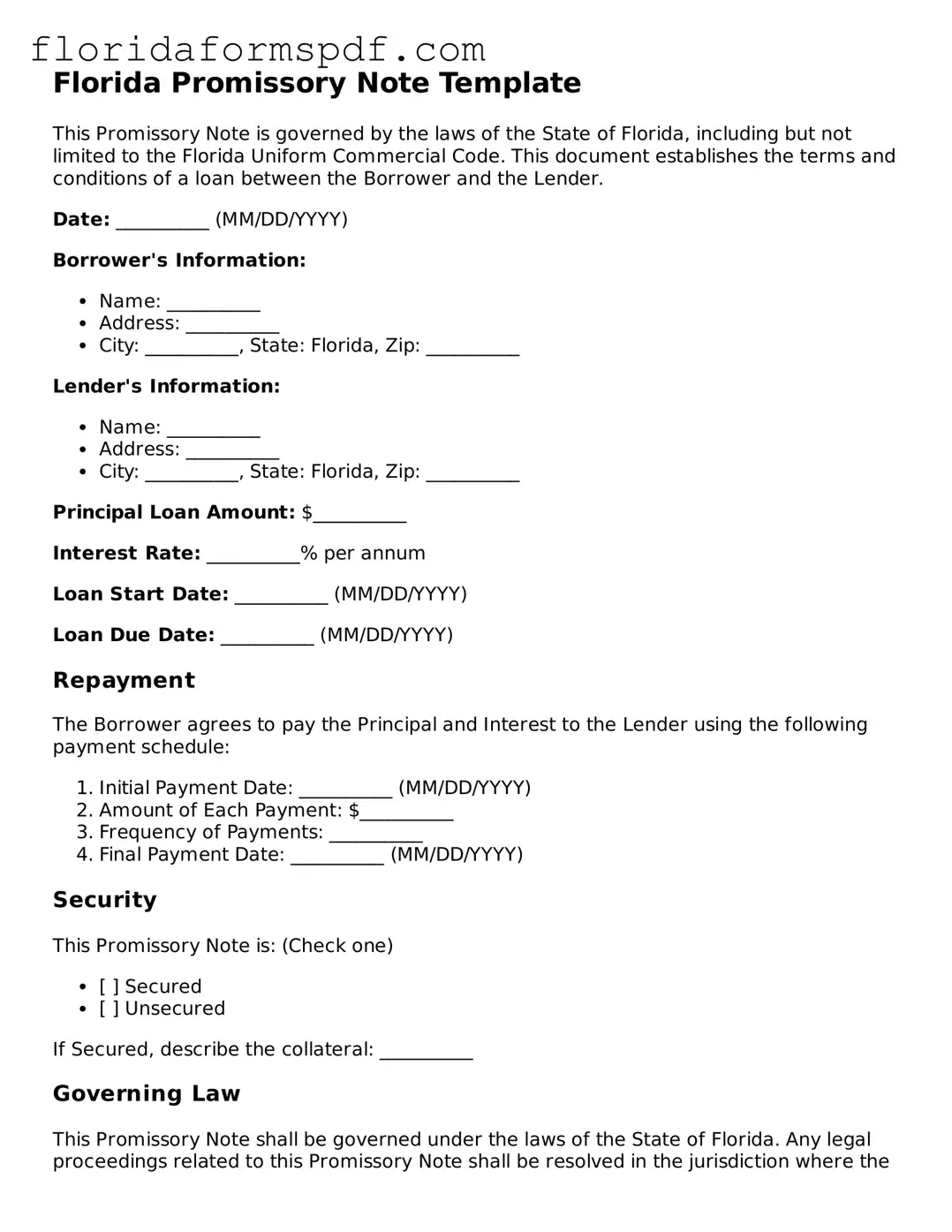

Florida Promissory Note Template

This Promissory Note is governed by the laws of the State of Florida, including but not limited to the Florida Uniform Commercial Code. This document establishes the terms and conditions of a loan between the Borrower and the Lender.

Date: __________ (MM/DD/YYYY)

Borrower's Information:

- Name: __________

- Address: __________

- City: __________, State: Florida, Zip: __________

Lender's Information:

- Name: __________

- Address: __________

- City: __________, State: Florida, Zip: __________

Principal Loan Amount: $__________

Interest Rate: __________% per annum

Loan Start Date: __________ (MM/DD/YYYY)

Loan Due Date: __________ (MM/DD/YYYY)

Repayment

The Borrower agrees to pay the Principal and Interest to the Lender using the following payment schedule:

- Initial Payment Date: __________ (MM/DD/YYYY)

- Amount of Each Payment: $__________

- Frequency of Payments: __________

- Final Payment Date: __________ (MM/DD/YYYY)

Security

This Promissory Note is: (Check one)

- [ ] Secured

- [ ] Unsecured

If Secured, describe the collateral: __________

Governing Law

This Promissory Note shall be governed under the laws of the State of Florida. Any legal proceedings related to this Promissory Note shall be resolved in the jurisdiction where the Borrower resides.

Signatures

Borrower's Signature: __________

Date: __________ (MM/DD/YYYY)

Lender's Signature: __________

Date: __________ (MM/DD/YYYY)

PDF Characteristics

| Fact | Description |

|---|---|

| 1. Definition | A Florida Promissory Note is a legal contract in which one party promises to pay a specific amount of money to another party under certain terms. |

| 2. Types | There are two main types: secured and unsecured. A secured note is backed by collateral, whereas an unsecured note is not. |

| 3. Governing Law | It is governed by Florida laws, including but not limited to, the Florida Uniform Commercial Code. |

| 4. Interest Rate | In Florida, the interest rate on a promissory note can't exceed the maximum lawful interest rates defined by state law. |

| 5. Usury Laws | Florida usury laws cap the interest rates and are important to consider when drafting a promissory note to avoid unlawful rates. |

| 6. Default | Terms of default should be clearly stated, including the consequences and any remedies available to the holder of the note. |

| 7. Co-signer Requirements | Co-signers may be required for unsecured notes, especially if the borrower's creditworthiness is questionable. |

| 8. Prepayment | Details regarding prepayment should be specified, including any penalties or allowances for paying the note early. | 8

| 9. Negotiability | The note should state whether it is negotiable, which would allow it to be transferred or sold to another party. |

| 10. Enforcement | If the borrower fails to meet the terms, the holder may enforce the note through appropriate legal actions, which are recognized under Florida law. |

Instructions on How to Fill Out Florida Promissory Note

When people borrow or lend money in Florida, they often use a Promissory Note to outline the repayment terms. This legal document ensures both the borrower and the lender understand their obligations. Completing the Florida Promissory Note form correctly is vital for ensuring that it's legally binding. The following steps are designed to help individuals complete the form accurately. By following them, one can ensure that all necessary details are included, making the agreement clear and enforceable.

- Start by stating the date the promissory note is being created at the top of the document.

- Write the full legal names and addresses of both the borrower and the lender in the designated sections.

- Specify the amount of money being loaned in U.S. dollars to make the amount clear and avoid any confusion.

- Detail the interest rate that will be applied to the loan. This should be a yearly rate.

- Describe the repayment plan. Include how often payments will be made (monthly, weekly, etc.), the amount of each payment, and the start date of the first payment. Also, clearly state the final due date by which the loan must be repaid in full.

- Include any provisions for late payments or penalties. This might involve additional fees or an increased interest rate if payments are not made on time.

- If applicable, describe any collateral that the borrower is using to secure the loan. Clearly identify the item or items and state that they are collateral.

- State any circumstances under which the loan may become due immediately. Common reasons might include the borrower's death or a breach of agreement terms.

- Both the borrower and the lender must sign and date the document. Witness signatures may also be required, depending on state laws and the specifics of the agreement.

- Keep the original document in a safe place and provide copies to both the borrower and the lender for their records.

Once the Florida Promissory Note form is fully filled out and signed, it becomes a legally binding document. It is crucial to keep a copy in a secure location and consider sharing a digital copy with a trusted advisor or attorney. Knowing the loan details are clearly outlined provides peace of mind to both the lender and the borrower, reinforcing the understanding and agreement between them. Proper completion and preservation of this document ensure that both parties are protected and aware of their responsibilities, paving the way for a straightforward and amicable repayment process.

Listed Questions and Answers

What is a Florida Promissory Note?

A Florida Promissory Note is a legal document that outlines a loan's terms between a borrower and a lender within the state of Florida. It serves as a promise by the borrower to pay back the borrowed money to the lender, according to the repayment conditions specified in the agreement. This document typically includes details such as the loan amount, interest rate, repayment schedule, and any other conditions agreed upon by the parties involved.

Is a Florida Promissory Note legally binding?

Yes, a Florida Promissory Note is a legally binding agreement between a borrower and a lender. Once both parties have signed the document, they are legally obligated to adhere to its terms. The note provides the lender with a legal pathway to pursue repayment through the court system if the borrower fails to meet the agreed-upon repayment terms.

Do I need to notarize a Florida Promissory Note?

While notarization is not strictly required for a Florida Promissary Note to be considered valid, it is highly recommended. Notarization adds an additional layer of verification and can help prevent disputes over the authenticity of the document. It also makes enforcing the note easier in court, should there be a need.

What information should be included in a Florida Promissory Note?

A proper Florida Promissory Note should include the full names and addresses of both the borrower and the lender, the amount of money being lent, the interest rate, repayment schedule (including dates and amounts), and any collateral securing the loan, if applicable. It should also detail the legal actions that can be taken if the borrower fails to repay the loan according to the terms.

Can I charge any interest rate on a loan under a Florida Promissory Note?

No, Florida law caps the amount of interest that can be charged on a loan. As of the current guidelines, the maximum allowable interest rate is set by statute and may change over time. It's important to review the most current regulations or consult with a legal professional to ensure compliance with state usury laws and to determine the maximum interest rate permitted at the time of the loan.

How can I enforce a Florida Promissory Note if the borrower fails to repay the loan?

If a borrower fails to repay the loan according to the agreed terms, the lender may take legal action to enforce the promissory note. This might involve filing a lawsuit to collect the debt. The court may then order the borrower to pay the loan amount, including any accrued interest and possibly court costs and attorney fees, depending on the circumstances. It's advisable to attempt all possible means of communication and negotiation before proceeding with legal action.

Are electronic signatures on Florida Promissory Notes valid?

Yes, electronic signatures are generally recognized as valid under both Florida law and federal law, provided they meet specific requirements. For an electronic signature to be considered valid, it must be executed in a manner that accurately records the parties’ agreement to the terms of the promissory note. Both parties must also consent to the electronic signing and retention of the document. Ensuring the e-signature process complies with applicable legislation is crucial for maintaining the document's enforceability.

Common mistakes

When individuals set out to fill the Florida Promissory Note form, the process may seem straightforward. However, certain oversights can lead to significant legal implications or misunderstandings in the future. It's important to approach this document with attentiveness to avoid common mistakes.

-

Not specifying the loan details clearly. One prevalent mistake is not being explicit about the amount of the loan and the repayment schedule. Detailed information, including the interest rate, total amount to be repaid, and the timeline for payments, needs to be distinctly laid out. Ambiguity in these terms can lead to disputes and potential legal challenges.

-

Forgetting to include the interest rate. The interest rate is a critical component of any promissory note, yet it is often overlooked or inaccurately recorded. In Florida, the interest rate must not exceed the statutory maximum; failing to specify this can render the note usurious and legally unenforceable.

-

Omitting default terms. Many people neglect to specify what constitutes a default and the repercussions following a default. It is essential to outline the circumstances under which the lender can demand full repayment of the outstanding loan amount and any applicable legal actions.

-

Not delineating between secured and unsecured loans. A crucial distinction in promissory notes is whether the loan is secured by collateral. Failure to clarify this aspect can lead to misunderstandings and complications, especially if the borrower defaults on the loan. Secured loans require a description of the collateral, which gives the lender a right to seize it if the loan is not repaid as agreed.

-

Lack of witness or notarization. While Florida law does not always require a promissory note to be witnessed or notarized, having the document notarized or witnessed can add an additional layer of protection and validity. Skipping this step can make it more challenging to enforce the promissory note if disputes arise.

Addressing these mistakes can help ensure that a promissory note is legally compliant and reduces the potential for future disputes. It is advisable to consult with a legal professional when preparing such important financial documents, to safeguard the interests of all parties involved.

Documents used along the form

In the realm of personal and business finance within Florida, a Promissory Note is a foundational document outlining the terms of a loan between a borrower and a lender. This agreement specifies the loan amount, interest rate, repayment schedule, and the consequences of non-payment. Accompanying and supporting this crucial document, several other forms and documents frequently play a vital role in ensuring the clarity, legality, and enforceability of financial transactions. Each of these documents serves a unique purpose, complementing and enhancing the protections and obligations established by the Promissory Note.

- Mortgage Agreement or Deed of Trust: This document is used when the loan is secured by real property. It grants the lender a lien on the property as security for the loan, defining the borrower's and lender's rights concerning the property.

- Security Agreement: For loans secured by personal property, a Security Agreement outlines which assets are being used as collateral. This ensures the lender can claim the collateral if the loan is not repaid.

- Guaranty: A Guaranty is a promise made by a third party (the guarantor) to pay the loan if the primary borrower fails to do so. It provides an additional layer of security for the lender.

- Loan Amortization Schedule: This detailed document breaks down each loan payment into principal and interest components over the loan term, providing a clear picture of how the loan balance decreases over time.

- Disclosure Statement: Required by federal and state laws, this document provides the borrower with critical information about the costs and terms of the loan, ensuring transparency.

- UCC-1 Financing Statement: For secured loans involving personal property, this form is filed with the state to publicly declare the lender's interest in the borrower's collateral, protecting the lender's rights.

- Late Payment Notice: This notice is sent to a borrower who is behind on their loan payments, detailing the amount due and any applicable late fees. It serves as a formal reminder to fulfill their obligation.

Together, these documents establish a comprehensive framework that governs the terms and conditions of a lending arrangement. By ensuring all necessary paperwork is accurately completed and duly filed, both lenders and borrowers can better protect their interests and navigate the complexities of financial transactions with greater confidence and security.

Similar forms

The Florida Promissory Note form is similar to other legal documents that formalize agreements between parties, particularly in emphasizing repayment terms and ensuring that all conditions are understood and accepted. These documents share common features in outlining the obligations of the parties, interest rates, repayment schedules, and consequences of default. Two such documents include loan agreements and IOUs, each serving distinct roles but overlapping in purpose with a promissory note.

Loan Agreement

A Loan Agreement is comprehensive and detailed, much like the Florida Promissory Note. Both documents specify the amount borrowed, the repayment schedule, interest rates, and the recourse in the event of default. However, a Loan Agreement goes a step further by typically including more extensive legal protections for both the lender and the borrower. It may also detail collateral requirements—something not always specified in a promissory note. Furthermore, Loan Agreements often involve legal representation and more formalities during the drafting process, making them more robust for larger loans.

IOU

An IOU (I Owe You) document, while less formal than a Florida Promissory Note, serves a similar basic purpose in acknowledging that a debt exists. Both documents record the amount owed and by whom, but the promissory note usually includes more detailed information such as repayment terms, interest rates, and what happens if the repayment conditions are not met. An IOU, on the other hand, is often a simpler declaration of debt without these extensive details. It's more of a casual reminder than a legally binding agreement, making it less comprehensive for legal enforcement compared to a promissory note.

Dos and Don'ts

When filling out the Florida Promissory Note form, it is essential to take care to ensure that the agreement is both legally binding and clearly understood by all parties involved. Here are some key dos and don'ts to consider:

- Do ensure the full legal names of both the borrower and the lender are clearly printed on the form to avoid any confusion about the parties involved.

- Do specify the loan amount in numbers and words to prevent discrepancies or misunderstandings about the total sum being lent.

- Do clarify the interest rate in accordance with Florida law to ensure that the terms are legal and enforceable.

- Do detail the repayment schedule, including dates and amounts, to provide a clear understanding of when the loan should be repaid.

- Do include the consequences of a default to inform the borrower of the legal implications of failing to meet the repayment terms.

- Don't leave any sections blank; if a section does not apply, mark it as "N/A" to indicate that it has been considered and deemed not applicable.

- Don't agree to an interest rate above the maximum allowed by Florida law, as doing so could render the promissory note unenforceable.

- Don't forget to have both parties sign and date the form, as the signatures validate the agreement and its terms.

- Don't neglect to keep a copy of the signed document for both the lender and borrower’s records, ensuring that both parties have proof of the agreement and its terms.

Misconceptions

When it comes to drafting or using a Florida Promissory Note form, there are several common misconceptions that can lead to confusion. Below, we will clarify some of these misunderstandings to help individuals navigate this financial instrument with more confidence.

- Misconception 1: A promissory note is the same as a loan agreement. While it's true that both pertain to borrowing money, a promissory note is a simpler document that details the borrower's promise to repay a sum to the lender. Loan agreements often include more detailed terms and conditions, such as clauses for arbitration and covenants.

- Misconception 2: Promissory notes do not need to be witnessed or notarized in Florida. Although Florida law does not mandate that promissory notes be witnessed or notarized, having these steps completed can add a layer of authentication and might be beneficial in the enforcement of the agreement.

- Misconception 3: You can only use a promissory note for personal loans between family and friends. Promissory notes can be used for a wide range of lending situations, including business loans, real estate transactions, and personal loans among various parties, not just family and friends.

- Misconception 4: Promissory notes are legally binding without consideration. Consideration, which is something of value exchanged between the parties, is a fundamental element required for any promissory note to be considered legally binding in Florida, as it is in other jurisdictions.

- Misconception 5: There is a standard, one-size-fits-all promissory note for use in Florida. Although you might find templates or generic promissory note forms, it is crucial to understand that the specifics of the note can and should be tailored to fit the particular needs and agreement between the lender and borrower.

- Misconception 6: Once signed, the terms of a promissory note are fixed and cannot be altered. The terms of a promissory note can be modified, but any changes should be agreed upon by all parties involved and, ideally, documented in a written amendment to the original note to avoid any future disputes.

- Misconception 7: Only financial institutions can issue promissory notes. While banks and other lending institutions commonly use promissory notes, any individual or entity can create and issue one, provided they comply with Florida's legal requirements.

Understanding these common misconceptions about Florida Promissory Notes can help ensure that individuals are better informed and can make more educated decisions when entering into such agreements. Proper knowledge and adherence to the law are crucial in navigating the financial and legal implications of these documents.

Key takeaways

When filling out and using a Florida Promissory Note form, it's essential to handle the process with care to ensure that all parties fully understand their obligations and rights under the agreement. Below are six key takeaways to consider:

Include all relevant information: Make sure to include all necessary details such as the names and addresses of the borrower and lender, the amount of money being borrowed, the interest rate, and the repayment schedule. This clarity helps prevent misunderstandings.

Understand the legal requirements: Florida has specific legal requirements for promissory notes, including the necessity for them to be in writing and include a promise to pay a specific sum of money to a named person or entity. Familiarizing yourself with these requirements ensures the document's enforceability.

Choose the right type of promissary note: There are two main types of promissory notes: secured and unsecured. A secured promissory note requires collateral to be pledged by the borrower, while an unsecured note does not. Selecting the appropriate type based on the agreement between the lender and borrower is crucial.

Define the repayment schedule clearly: The repayment schedule should be outlined in detail within the note, including due dates for payments and whether interest will be compounded or simple. Accurately defining these terms helps both parties manage their expectations and responsibilities.

Consider the implications of late payments or default: It's important to specify the consequences of late payments or defaulting on the loan. This includes any late fees, higher interest rates, or legal actions that might be taken. Both the lender and borrower should understand these implications fully.

Signatures are crucial: For a promissory note to be legally binding in Florida, it must be signed by both the borrower and the lender. It's also recommended to have the signatures notarized to add an extra layer of authenticity and protection against disputes.

Popular Florida Templates

Contract for Contractors - Defines the scope of the agreement, ensuring that all parties have a shared understanding of the services to be provided.

General Release of Liability Form Florida - In some cases, a Release of Liability can also cover property damage, in addition to personal injury, depending on the activities involved and the terms of the agreement.