Fill Out a Valid Rt 6A Florida Template

Understanding the intricacies of the Rt 6A Florida form, an essential document issued by the Florida Department of Revenue, is a vital responsibility for every employer in the state. This form serves as the Employer’s Quarterly Report Continuation Sheet, a crucial component for those required to file quarterly tax/wage reports. It bears significance not only for its role in tax administration but also for the legal obligation it imposes on employers to report employment activity and wages paid within the quarter, regardless of whether any taxes are due. The form distinctly outlines the requirement for employers to furnish Social Security numbers (SSNs) for employees, ensuring these identifiers serve as the backbone for managing Florida's tax obligations efficiently. Highlighting the confidentiality and protected nature of these SSNs under sections 213.053 and 119.071, Florida Statutes, it echoes the state's commitment to privacy. The document stresses the legality behind the collection of SSNs, backed by state and federal law, directing users to the state website for a deeper understanding of privacy rights and obligations. Moreover, it details the method for reporting each employee's wages, emphasizing the initial $7,000 of wages paid to an employee within a calendar year as taxable, a piece of information pivotal for accurate tax reporting. Crafted under the regulations set forth by TC Rule 73B-10.037 of the Florida Administrative Code, this form encapsulates a blend of compliance, confidentiality, and administrative necessity, making it indispensable for the proper functioning of any entity engaged in employment practices within the Sunshine State.

Document Preview Example

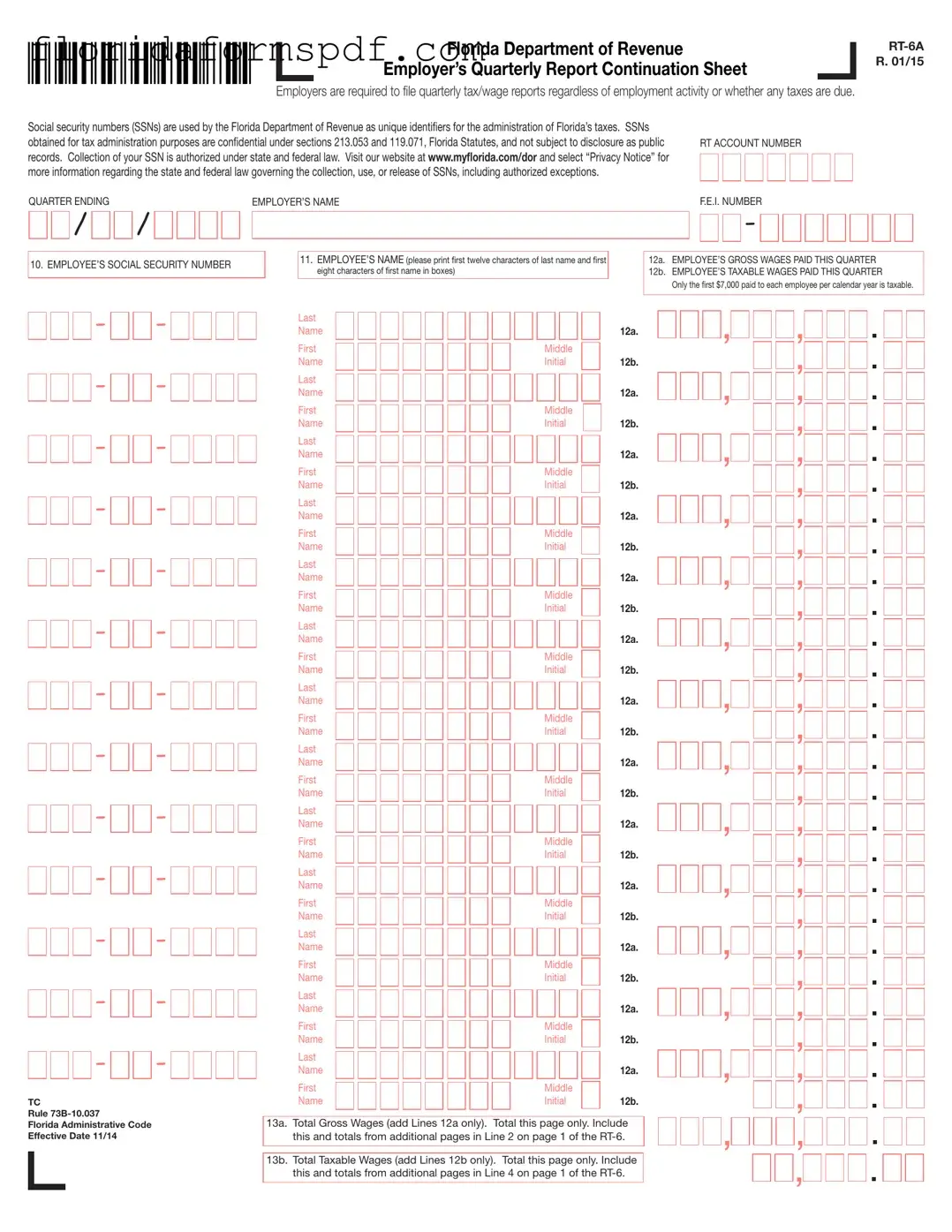

Florida Department of Revenue

Employer’s Quarterly Report Continuation Sheet

Employers are required to ile quarterly tax/wage reports regardless of employment activity or whether any taxes are due.

Social security numbers (SSNs) are used by the Florida Department of Revenue as unique identiiers for the administration of Florida’s taxes. SSNs

obtained for tax administration purposes are conidential under sections 213.053 and 119.071, Florida Statutes, and not subject to disclosure as public RT ACCOUNT NUMBER records. Collection of your SSN is authorized under state and federal law. Visit our website at www.mylorida.com/dor and select “Privacy Notice” for

more information regarding the state and federal law governing the collection, use, or release of SSNs, including authorized exceptions.

QUARTER ENDING |

EMPLOYER’S NAME |

F.E.I. NUMBER |

/

/

/

-

-

10. EMPLOYEE’S SOCIAL SECURITY NUMBER

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

TC

Rule

Florida Administrative Code

Effective Date 11/14

11. EMPLOYEE’S NAME (please print irst twelve characters of last name and irst eight characters of irst name in boxes)

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

Last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Middle |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial |

|

|

12b. |

||

13a. Total Gross Wages (add Lines 12a only). Total this page only. Include this and totals from additional pages in Line 2 on page 1 of the

13b. Total Taxable Wages (add Lines 12b only). Total this page only. Include this and totals from additional pages in Line 4 on page 1 of the

12a. EMPLOYEE’S GROSS WAGES PAID THIS QUARTER

12b. EMPLOYEE’S TAXABLE WAGES PAID THIS QUARTER

Only the irst $7,000 paid to each employee per calendar year is taxable.

Document Overview

| Fact Name | Description |

|---|---|

| Form Designation | RT-6A |

| Issuing Authority | Florida Department of Revenue |

| Form Purpose | Employer’s Quarterly Report Continuation Sheet |

| Reporting Requirement | Employers must file quarterly tax/wage reports regardless of employment activity or whether any taxes are due. |

| Use of Social Security Numbers | Used as unique identifiers for the administration of Florida’s taxes, and their collection is confidential and authorized under state and federal law. |

| Confidentiality of SSNs | Confidential under sections 213.053 and 119.071, Florida Statutes, not subject to public records disclosure. |

| Governing Law | Sections 213.053 and 119.071, Florida Statutes; TC Rule 73B-10.037 Florida Administrative Code |

| Privacy Notice | Details about the collection, use, or release of SSNs, including exceptions, are available on the Florida Department of Revenue website. |

| Taxable Wage Base | Only the first $7,000 paid to each employee per calendar year is taxable. |

| Form Revision Date | January 2015 (01/15) |

Instructions on How to Fill Out Rt 6A Florida

Filling out the Rt 6A Florida form correctly is a crucial next step for employers. This continuation sheet helps in reporting quarterly tax and wage details accurately to the Florida Department of Revenue. Timely and precise filling ensures compliance with state regulations and contributes to the streamlined processing of tax-related matters. For those who are navigating this form for the first time or need a reminder, detailed step-by-step instructions are provided below.

- Begin by entering the RT Account Number at the top of the form. This number is unique to your business and is found on previous correspondence from the Florida Department of Revenue.

- Fill in the Quarter Ending date as mm/dd/yyyy to indicate which quarter you are reporting for.Type the Employer’s Name as registered with the Florida Department of Revenue.

- Enter the F.E.I. Number (Federal Employer Identification Number) specific to your business.

- The next section requires detailed employee information. For each employee, start by entering the Employee’s Social Security Number.

- In the boxes provided under Employee’s Name, print the first twelve characters of the last name and first eight characters of the first name ensuring clarity and legibility.

- For 12a. Employee’s Gross Wages Paid This Quarter, input the total gross wages paid to the employee during the reported quarter.

- Under 12b. Employee’s Taxable Wages Paid This Quarter, note that only the first $7,000 paid to each employee per calendar year is taxable. Fill in the taxable wage amount accordingly.

- Repeat steps 5 through 8 for each employee on your workforce during the quarter.

- To find the Total Gross Wages, add all the amounts entered in 12a for each employee and place the total in 13a. This is the sum of gross wages paid this quarter.

- Similarly, calculate the Total Taxable Wages by summing up the figures entered in 12b for each employee. Record this total in 13b.

- Remember to include the totals from 13a and 13b in the respective lines on page 1 of the RT-6.

After completing the form, ensure to review all the information for accuracy. Misreported or illegible information can lead to processing delays or potential issues with the Florida Department of Revenue. Submit the completed form by the designated deadline to maintain compliance and avoid any late submission penalties.

Listed Questions and Answers

What is the RT-6A Florida form used for?

The RT-6A Florida form is a continuation sheet that employers in Florida use to report quarterly tax and wage details for their employees to the Florida Department of Revenue. This form assists in providing additional information that does not fit on the primary Employer’s Quarterly Report (RT-6). It is essential for the accurate and comprehensive reporting of each employee's social security number, name, gross wages paid during the quarter, and taxable wages.

Who needs to file the RT-6A form?

All employers in Florida who have more employees than can be reported on the main RT-6 form need to file the RT-6A form. This is a requirement for every quarter in which they have paid wages to their employees, regardless of whether there has been any change in employment activity or if any taxes are due.

How often should the RT-6A form be filed?

The RT-6A form should be filed quarterly, along with the RT-6 form. The due dates for these reports are April 30, July 31, October 31, and January 31, covering the previous quarter’s payroll information.

Is there a penalty for not filing the RT-6A form?

Yes, employers who fail to file the RT-6A form on time may face penalties. These penalties are in addition to any that may be assessed for not filing the RT-6 form or for not paying any taxes due. It is crucial to file all required forms and pay any associated taxes by the due dates to avoid penalties.

Can the RT-6A form be filed electronically?

Yes, the RT-6A form, alongside the RT-6 form, can be filed electronically. Employers are encouraged to use the Florida Department of Revenue’s website for electronic submissions, which offers a more efficient and faster processing method than paper filings.

What information is needed to complete the RT-6A form?

To complete the RT-6A form, an employer must provide each employee's social security number, first name (first eight characters), and last name (first twelve characters). Additionally, the gross wages paid to each employee during the quarter and the taxable wages must be reported. Only the first $7,000 paid to an employee per calendar year is considered taxable.

Are social security numbers required for the RT-6A form?

Yes, employers must provide social security numbers for each employee reported on the RT-6A form. These numbers are used by the Florida Department of Revenue as unique identifiers for the administration of Florida’s taxes. The collection and use of social security numbers are governed by state and federal laws, ensuring the confidentiality and protection of this information.

What should be done if an error is found after the RT-6A form has been submitted?

If an employer discovers an error in a previously submitted RT-6A form, they should correct the mistake and refile the form as soon as possible. The Florida Department of Revenue provides guidelines on how to amend reports, and employers may need to provide a detailed explanation of the correction.

Is it necessary to file the RT-6A form if no wages were paid during the quarter?

Yes, employers are required to file the RT-6 and RT-6A forms each quarter, regardless of whether any wages were paid. The forms should be filed with the necessary sections completed, indicating that no wages were paid during the reporting period, to remain compliant with filing requirements.

Where can more information or assistance be found regarding the RT-6A form?

For more information or assistance with the RT-6A form, employers can visit the Florida Department of Revenue’s website at www.myflorida.com/dor. The website provides comprehensive resources, including a Privacy Notice that covers the collection, use, and release of social security numbers, as well as guidelines for filing and amendments. Additionally, employers may contact the department directly for personalized assistance.

Common mistakes

Filling out the RT-6A Florida form, known as the Employer’s Quarterly Report Continuation Sheet, is a critical task for employers. However, it's easy to make mistakes if you're not careful. Here are four common mistakes to avoid:

Incorrect Social Security Numbers (SSNs): One of the most common mistakes is entering an employee's SSN incorrectly. Since the Florida Department of Revenue uses SSNs as unique identifiers for tax administration, any error in these numbers can lead to misidentified employees and processing delays.

Not Following Name Entry Format: The form requires the first twelve characters of the employee's last name and the first eight characters of the first name in specific boxes. Failing to adhere to this format can result in inaccuracies in record-keeping and potential issues in employee identification for tax purposes.

Miscalculating Wages: Employers must report both the total gross wages and the taxable wages paid to each employee during the quarter. It's crucial to remember that only the first $7,000 paid to each employee per calendar year is taxable. Errors in calculating either gross or taxable wages can lead to incorrect tax payments or filings.

Not Including Totals From Additional Pages: If you're using more than one RT-6A form due to having numerous employees, it's essential to include the total gross wages and taxable wages from all pages in the relevant sections on page 1 of the RT-6. Overlooking this detail can lead to underreporting or overreporting wages.

By avoiding these mistakes, employers can ensure smoother processing of their quarterly tax/wage reports and stay in compliance with Florida's tax administration requirements.

Documents used along the form

The process of managing and submitting the Florida Department of Revenue Employer’s Quarterly Report, symbolized by the RT-6A form, is a multifaceted task that necessitates the inclusion of a suite of complementary documents for streamlined tax and wage reporting. These documents, typically used alongside the RT-6A form, play crucial roles in ensuring employers fulfill their reporting responsibilities accurately and comprehensively under Florida’s tax administration framework.

- RT-6 Form - The primary Employer’s Quarterly Report filed by employers. It provides a summary of wages paid, taxes withheld, and due for all employees. This form establishes the context and figures that the RT-6A form continues or elaborates upon.

- Form W-2 - The Wage and Tax Statement provided to each employee and the IRS at year-end. It details the employee's annual wages and the amount of taxes withheld from their paycheck. These figures are necessary for completing both the RT-6 and RT-6A forms.

- Form W-4 - Employee's Withholding Certificate used by employers to determine the amount of federal income tax to withhold from employees' wages. While it is more directly related to payroll processing, the information ensures the accuracy of tax withholding figures reported on the RT-6 and RT-6A forms.

- Form W-9 - Request for Taxpayer Identification Number and Certification. This form is used to gather information from contractors or freelancers, which is vital for the RT-6A when reporting payments to non-employees, should it be applicable.

- UCB-412 - Employer’s Quarterly Report of Wages Paid to Each Employee. Similar to the RT-6A, this form is required by some states and contains detailed information about wages paid. For Florida employers, maintaining similar records can aid in the accuracy of reporting on the RT-6A form.

- Form 940 - Employer's Annual Federal Unemployment (FUTA) Tax Return. This IRS form calculates the employer's federal unemployment tax liability. While it is an annual requirement, the information provided helps reconcile the quarterly data reported on both RT-6 and RT-6A forms regarding unemployment taxes.

In sum, these documents serve as integral components of the employment tax reporting and wage declaration ecosystem in Florida. Collectively, they facilitate a comprehensive and substantive approach to fulfilling the reporting obligations laid out by the Florida Department of Revenue, ensuring employers remain compliant with state and federal tax laws. Furthermore, they underscore the interconnectedness of various reporting frameworks, highlighting the necessity for meticulous record-keeping and data consistency across all forms and reports filed by an employer.

Similar forms

The Rt 6A Florida form is similar to various other documents utilized for reporting employee wages and taxes, all of which serve the purpose of ensuring proper documentation and compliance with related laws. These documents include the Federal Form 941, State Unemployment Insurance (SUI) Reports, and New Hire Reporting forms. Each has its unique elements but fundamentally aims at capturing data essential for tax calculation and compliance.

Federal Form 941, Employer's Quarterly Federal Tax Return, is akin to the Rt 6A in that it requires employers to report wages paid, taxes withheld from employees, and the employer's portion of social security and Medicare taxes. Both forms are submitted quarterly and play a crucial role in maintaining accurate tax records. The main difference lies in their jurisdictional use; Form 941 is a federal requirement, whereas the Rt 6A is specific to the state of Florida. Each form facilitates the collection of taxes critical for funding government programs.

State Unemployment Insurance (SUI) Reports share similarities with the Rt 6A form because they both require information on employee wages. These reports determine the employer's state unemployment tax liability. Like the Rt 6A, SUI reports are filed on a quarterly basis and are essential for managing unemployment insurance funds. The details reported help in calculating the amount an employer owes to the state unemployment insurance pool, from which benefits are paid out to eligible unemployed workers. Although focused on different aspects of employment-related expenditures, both are pivotal in labor force management and compliance.

New Hire Reporting forms are designed to collect information on newly hired employees and, like the Rt 6A, include particulars such as the employee's name, address, and social security number. While the Rt 6A is broad, focusing on quarterly wage and tax reporting for all employees, New Hire Reports are specifically for informing state agencies about additions to the workforce. This reporting helps in locating parents who owe child support. Despite the difference in their primary objectives, both forms ensure employees are properly documented and contribute to the overarching goal of compliance and efficient administration of public policies.

Dos and Don'ts

When completing the Rt 6A Florida form, it's important to pay close attention to detail and follow specific guidelines to ensure accurate and efficient processing. Here are several do's and don'ts to consider:

- Do ensure all employee details are filled in accurately. Double-check social security numbers, names, and wage amounts for each employee.

- Do not leave any fields blank. If a section does not apply, fill in "N/A" (not applicable) or "0" (zero) if it concerns financial figures.

- Do use the correct format when entering dates and social security numbers to avoid processing delays.

- Do not estimate wage amounts. Use exact figures to report gross wages paid and taxable wages for each employee.

- Do add totals from all continuation sheets (if applicable) and include them on the first page of the RT-6 form as instructed.

- Do not exceed the space provided. If the first name or last name does not fit within the designated boxes, use the first twelve characters of the last name and the first eight characters of the first name only.

- Do remember that only the first $7,000 paid to each employee per calendar year is taxable. Accurately calculate this for the “Total Taxable Wages” column.

- Do not disregard the privacy notice regarding the collection, use, or release of social security numbers. Be aware that providing this information is both authorized and protected under state and federal laws.

- Do visit the Florida Department of Revenue's website for more information on how to properly fill out and submit the form should you have any questions or need clarification.

Following these guidelines will help ensure that the form is completed correctly and efficiently, reducing the chance of errors and the possibility of having to resubmit the form.

Misconceptions

When it comes to the RT-6A Florida form, a series of misunderstandings frequently arises among employers who are tasked with navigating these filings. Let's clear up some of the most common misconceptions.

- Employers are only required to file the RT-6A if they owe taxes. This is incorrect. Each quarter, employers must submit the RT-6A, regardless of their tax situation or employment activity. This form is essential for maintaining accurate records with the Florida Department of Revenue.

- Social Security numbers (SSNs) submitted can be disclosed publicly. This is a misunderstanding. SSNs collected via the RT-6A are confidential and protected under federal and state laws, specifically sections 213.053 and 119.071 of the Florida Statutes. These numbers are exclusively used for tax administration purposes.

- The form can be disregarded if an employer has not hired new employees. This is a misconception. The obligation to file the RT-6A is not dependent on whether new employees were hired within the quarter. It is a report of employee earnings and tax information that must be filed every quarter, regardless of changes in the workforce.

- Employers need to report wages beyond the first $7,000 paid to each employee. This is not accurate. The RT-6A specifically requires reporting only the first $7,000 of wages paid to each employee within the calendar year. Amounts beyond this are not considered taxable for this particular reporting purpose.

- Personal names can be entered without limitation on characters. There is a specific format required for names on the RT-6A form. This form limits the entry to the first twelve characters of the last name and the first eight characters of the first name, ensuring consistency and avoid errors in identity verification processes.

- Any issues related to the collection, use, or release of SSNs are not addressed or governed by law. This is false. The collection and use of SSNs are governed by both state and federal laws, with detailed privacy notices available to clarify the legal framework and the authorized exceptions concerning SSN disclosure. Employers and employees alike are encouraged to understand these protections.

Dispelling these misconceptions is vital for employers to accurately fulfill their reporting obligations and ensure the confidentiality and correct treatment of employee information according to legal requirements.

Key takeaways

When dealing with the RT-6A Florida form, it's important to remember that this document serves as a continuation sheet for the Employer’s Quarterly Report, which is required by the Florida Department of Revenue. Below are key takeaways to ensure accurate and compliant submissions:

- Quarterly Filing Requirement: Employers must file quarterly tax/wage reports using the RT-6A form as part of their ongoing obligations, regardless of their level of employment activity or if they owe any taxes for that quarter.

- Use of Social Security Numbers (SSNs): The Florida Department of Revenue uses SSNs as unique identifiers for tax administration purposes. The collection and use of SSNs on the RT-6A are backed by both state and federal laws, emphasizing the importance of handling this information with care to maintain confidentiality.

- Details Required for Each Employee: For every employee, the employer must report the employee’s SSN, the first twelve characters of the employee’s last name, and the first eight characters of the employee’s first name. This level of detail helps in accurately identifying individuals for tax purposes.

- Gross vs. Taxable Wages: The RT-6A form requires employers to distinguish between total gross wages paid and taxable wages paid to each employee within the quarter. It’s crucial to note that only the first $7,000 paid to each employee per calendar year is taxable, which affects how these amounts are calculated and reported.

- Compilation of Totals: Employers must compile total gross wages and total taxable wages separately. These totals should reflect the sum of wages for all listed employees on the continuation sheet. Additionally, these totals must be included in specific lines on page 1 of the primary RT-6 form, ensuring the comprehensive reporting of employer wage liabilities and contributions.

Accurately filling out and submitting the RT-6A form is a crucial aspect of an employer's compliance with Florida's tax administration. Paying close attention to the details required on this form ensures that the process is carried out effectively, maintaining the confidentiality and accuracy of employee data and contributing to the smooth operation of tax-related responsibilities.

Popular PDF Documents

Florida Lottery Claim - Winners must complete this form to receive their winnings, whether large or small.

What Happens at an Injunction Hearing - Guides individuals through the process of officially requesting changes to an existing injunction, helping maintain relevance and effectiveness.

Florida Notice to Owner Form - An informative alert for Florida property owners, underscoring their risk of facing liens if contractors and suppliers remain unpaid.